Statistics on Pensioners in Finland

Statistics on Pensioners in Finland includes data on all recipients of earnings-related and national pensions, new pension recipients and pension expenditure. The data on pension recipients living in Finland and abroad are presented separately. The statistics is produced in co-operation with the Social Insurance Institution of Finland (Kela).

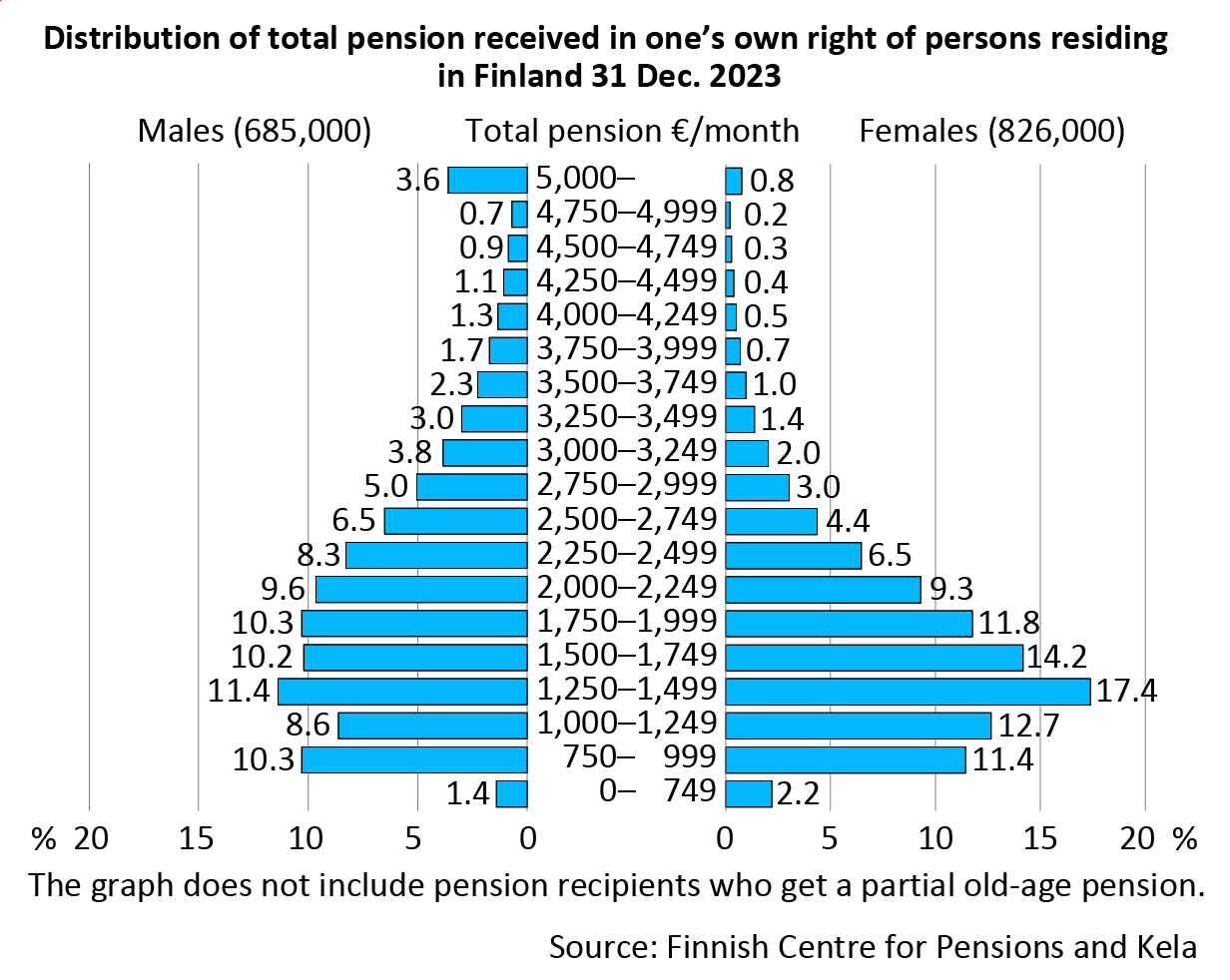

Average total monthly pension 1,977 euros

The average total monthly pension of pension recipients in Finland in 2023 was 1,977 euros. Women received an average monthly pension of 1,779 euros and men 2,216 euros. The median monthly pension was 1,736 euros.

Almost two in three pension recipients received a monthly pension of less than 2,000 euros. 70 per cent of women and 52 per cent of men received a monthly pension of less than 2,000 euros. 12 per cent of all pension recipients received a monthly pension of more than 3,000 euros.

(Updated on 27 March 2024)

Read more:

Latest publications:

Tables in statistical database of the Finnish Centre for Pensions:

- Number of pension recipients

- Size of pension recipients’ pension

- Share of population receiving a pension

- Pension recipients living abroad

- Number of new retirees

- Size of new retirees’ pension

Tables and graphs in Key Figures:

- Number of pension recipients

- Share of population receiving a pension

- Average total pension

- Pensions paid abroad

Statistical services provides further information:

Statistics on Pensioners in Finland

Producers: Finnish Centre for Pensions and the Social Insurance Institution of Finland

Website: Statistics on Pensioners in Finland

Subject area: Social security

Part of the Official Statistics of Finland (OSF): Yes

Description

The statistics offers a general overview of recipients of earnings-related and national pensions in Finland.

Data content

The statistics includes data on all recipients of earnings-related and national pensions and also new pension recipients.

The data on pension recipients living in Finland and abroad are presented separately.

Classification

Pension scheme; pension benefit; pension amount; gender, age, nationality and country of residence of pension recipient; disease classification ICD-10; regional classification: municipality, province

Methods of data collection and source

The statistics is based on the registers of the Finnish Centre for Pensions and the Social Insurance Institution of Finland.

Update frequency

Once a year.

Time of completion or release

The statistics on pension recipients is released in the spring following the statistical year. The data on new retirees is released in year after the statistical year. For a more detailed schedule, consult the Release Calendar

Time series

The statistics has been released since 1981. The statistics has been supplemented with data on new retirees as of 2001.

For the main part, the time series of the statistics are comparable. The Quality Description (section “Coherence and comparability of data”) of the statistics includes more detailed information on the comparability of the time series.

Key words

social insurance, pension, earnings-related pension, national pension, old-age pension, disability pension, unemployment pension, farmers’ special pension, part-time pension, survivors’ pension, retirement

Concepts and definitions

Statistical units

Pension recipient

A pension recipient is a person who gets a pension in their own right or a survivors’ pension on the last day of the year of statistics. One person may get simultaneously pensions both under several different pension acts and of several different types.

Persons getting a pension in their own right get old-age, partial old-age, disability, unemployment or part-time pensions, or special pensions for farmers.

All pension recipients include persons who get pensions in their own right as well as the recipi-ents of survivors’ pensions.

A person who simultaneously gets a pension paid by Kela and an earnings-related pension is a person who gets a pension under review from both schemes. For example, in the table for disability pension recipients, the pension from both schemes must be a disability pension.

New retiree

A new retiree is a person whose pension in their own right (other than a part-time or a partial old-age pension) started during the year of statistics. A further criterion is that the person has not received a pension in their own right (excluding a part-time and a partial old-age pension) for at least two years. A person is considered a new retiree from the earnings-related or nation-al pension scheme during the year in which the transfer from said scheme took place. The cri-terion for all new retirees is that they have not received pension in their own right from either scheme for at least two years.

Persons who have started to get a part-time or a partial old-ge pension are not considered to be retired, so they are not included in the total number of new retirees. They will noo be included in the number of new retirees until the year in which they start to get some other pension in their own right.

Factors describing the pension recipients

Age

The pension recipient’s age is the age at the end of the year of statistics. A new retiree’s age is, in general, the person’s age when the pension starts. When calculating the share of new retirees in the population per age group, the person’s age at the end of the year of statistics is used.

The average age is the arithmetic mean of the ages of new retirees.

The median age is the observation at the mid-point of the material, i.e. half of the new retirees are younger than the median age and the other half are older.

Average pension

All monetary amounts given in the statistics are gross monthly pensions.

The pension can be made up of an earnings-related pension, a national pension paid by Kela, special provision benefits relating to these pensions, or a guarantee pension. The average pension is the arithmetic mean of the gross pensions.

The average pension in one’s own right of those who get a pension in their own right includes the euro amount of the pensions in one’s own right (excluding part-time and partial old-age pensions). The average pension in one’s own right of new retirees is calculated as the average value of pensions that began during the year and were in force on the last day of the year. The calculations do not include pensions that both began and ended during the year.

The average total pension of those who get a pension in their own right includes, besides the aforementioned, also the amount of survivors’ pensions and the amount of guarantee pen-sions, child increases and front-veterans’ supplements paid by Kela.

The average survivors’ pension of the recipient of a survivors’ pension only includes the euro amount of the survivors’ pension, and the average total pension includes all benefits paid as pensions to the recipient of a survivors’ pension

Illness

The categorizing of persons receiving disability pension or having retired on disability pension by disease is based on the main disease which is the basis of the pension. The data on diseases is primarily based on the diagnosis of the earnings-related pension scheme.

The main groups and some subgroups of diseases are shown for the diseases.

Since 1996, the diagnoses and the corresponding codes are based on the ICD 10 classification of diseases. Disability pensions granted before 1996 are based on the previous ICD 9 classification. The codes according to the old classification have been as closely as possible placed in the correct category in the new classification.

Regional division

In the statistic, regions are categorized based on the regional categorization valid at the end of the year of statistics. The domicile of a person equals the domicile of the last day of the year of statistics. Data on domiciles is available from the population data of Kela.

In the statistic, countries of residence are categorized based on the country categorization valid at the end of the year of statistics. In pensions paid abroad, the person’s country of residence is the country of residence on the last day of the year of statistics. Data on country of residence is available from the population data of Kela, completed with information received from the pension providers.

Citizenship

Citizenship is categorized based on the currently valid citizenship at the end of the year of statistics. The citizenship data is acquired from Kela’s population data and completed with information received from the pension providers.

Population share

Population shares of pension recipients are calculated for pension recipients resident in Finland in per cent of the population insured for national social security benefits. The population more or less covers the resident population of the country but includes also Finnish citizens tempo-rarily living abroad.

1. Contact

1.1 Contact organisation

The Finnish Centre for Pensions and the Social Insurance Institution of Finland (Kela).

1.2 Contact organisation unit

Finnish Centre for Pensions: Planning Department, Kela: Information Services.

1.3 Contact name

Joonas Hautamäki (Finnish Centre for Pensions)

Jari Kannisto (Finnish Centre for Pensions)

Reeta Pösö (Kela)

1.4 Contact person function

Statistical expert

1.5 Contact mail address

The Finnish Centre for Pensions

FI-00065 ELÄKETURVAKESKUS

Finland

1.6 Contact email address

firstname.lastname@etk.fi

firstname.surname@kela.fi

Contact form (Finnish Centre for Pensions)

1.7 Contact phone number

+358 29 411 20 (Finnish Centre for Pensions)

1.8 Contact fax number

Fax: +358 9 148 1172 (Finnish Centre for Pensions)

2. Metadata update

2.1. Metadata last certified

27 March 2024

2.2. Metadata last posted

27 March 2024

2.3. Metadata last update

27 March 2024

3. Statistical presentation

3.1. Data description

The statistics describe the number and average pensions of persons who have received pensions from the Finnish earnings-related and national pension schemes and those who have retired.

3.2. Classification system

Pension scheme; pension benefit; pension amount; gender and age of pension recipient; disease classification ICD-10, regional classification: municipality, province, wellbeing services county and country of residence.

3.3. Sector coverage

The statistics cover all statutory pensions from the Finnish earnings-related and national pension schemes. It combines the pensions a person receives from different sources.

3.4. Statistical concepts and definitions

Concepts and definitions have been presented on the statistics page.

3.3. Statistical unit

Person / pension recipient.

3.6. Statistical population

Persons receiving a pension from the Finnish earnings-related and national pension schemes.

3.7. Reference area

Municipality, province, wellbeing services county and country of residence.

3.8. Time coverage

Basic data are available from 1981 onwards. Data on retired persons are available from 2001 onwards.

4. Unit of measure

Number of persons.

Amount of pension: €/month (gross).

Share of population: % of population covered by Kela social insurance.

5. Reference period

For pension recipients, the last day of the statistical year. For retired persons, the calendar year.

6. Institutional mandate

6.1. Legal acts and other agreements

Both the Finnish Centre for Pensions and Kela are obliged to compile statistics. The Act on the Finnish Centre for Pensions states that the Finnish Centre for Pensions is responsible for statistical activities within its field of competence. Similarly, the Act on the Social Insurance Institution states that Kela is responsible for compiling statistics, estimates and forecasts.

6.2. Data sharing

The same datasets are shared between the Finnish Centre for Pensions and Kela. Part of the data is also sent to Statistics Finland, for example for employment statistics.

Statistical data are sent annually to the NOSOSCO group for social benefits and to the Finnish Institute of Health and Welfare for the European System of Integrated Social Protection Statistics (ESSPROS).

7. Confidentiality

7.1. Confidentiality – policy

The Finnish Centre for Pensions is committed to data protection as a fundamental principle of statistics, which ensures the confidentiality of data.

7.2. Confidentiality – data treatment

Data is protected by the necessary physical and technical solutions at the various stages of processing. Personnel have access only to the data necessary for their work. Third parties do not have access to the premises where the data is processed. Employees are required to sign a confidentiality agreement when they are hired.

8. Release Policy

The Statistical Yearbook on Pensioners in Finland is a joint statistics produced by the Finnish Centre for Pensions and Kela and released on the website of the Finnish Centre for Pensions.

The statistics of the Finnish Centre for Pensions are released on weekdays at 9.00 a.m. on the website of the Finnish Centre for Pensions. Any exceptions to the release time are announced separately.

The data in the statistical database are released as open data. The database’s open interface can be freely used under the CC BY 4.0 licence, with the Finnich Centre for Pensions being cited as the source of the statistical data.

8.1. Release Calendar

The release dates of the statistics are published in the release calendar. The release calendar for the following year is published towards the end of the year.

8.2. Release calendar access

8.3. User access

The statistics are available to everyone when they are published on the website of the Finnish Centre for Pensions at a previously announced date.

Embargo policy: Media that are bound by the journalist’s guidelines may request material from the Finnish Centre for Pensions’ Communications Department.

9. Frequency of dissemination

Data on retired persons are published in March each year. Data on new retirees are published in June.

A separate publication is issued each autumn.

10. Accessibility and clarity

10.1. News release

The publications of the statistics can be found in the shared open repository Julkari: Statistical Yearbook of Pensioners in Finland 2023

Press releases on this topic can be found online at the website of the statistics.

Statistics on pensioners in Finland (Julkari)

10.2. Publications

Statistical yearbook of pensioners in Finland (Julkari)

Statistical yearbook of pensioners in Finland, 2004–2017 (Julkari)

10.3. Online database

Number of pension recipients (PxWeb)

Number of new retirees (PxWeb)

Size of pension recipients’ pension (PxWeb)

Size of new retirees’ pension (PxWeb)

Share of population receiving a pension (PxWeb)

Pension recipients living abroad (PxWeb)

10.4. Microdata access

At the Finnish Centre for Pensions, we can extract research material from our registers for scientific research. We disclose the data in compliance with the principles of the Act on the Openness of Government Activities and the Data Protection Act. As a rule, we do not disclose register data for commercial purposes. The scientific research must be identified.

Apply for research access to register data of the Finnish Centre for Pensions (pdf)

11. Quality Management

11.1. Quality assurance

The Finnish Centre for Pensions is committed to the quality principles of Official Statistics of Finland. Our statistical production follows the quality criteria of Official Statistics of Finland, which are compatible with the European Statistics Code of Practice.

11.2. Quality assessment

The quality of statistics is assessed at several stages in the statistical process.

12. Relevance

12.1. User needs

Feedback from users is gathered through customer surveys. Feedback is also collected through direct contact. The feedback received is monitored and taken into account in the development of the statistics.

13. Accuracy and reliability

13.1. Overall accuracy

The data are based on administrative registers. The source data are at individual level and used for the payment of pensions.

13.2. Sampling error

–

13.3. Non-sampling error

The register data are extracted at the beginning of the year, when some of the retroactive pension decisions may be missing from the statistical data.

14. Timeliness and punctuality

14.1. Timeliness

The statistical data are produced in several parts, which are published in three separate releases after the data quality check.

The first part is published in March of the year following the statistical reference year and the last part in September.

15. Coherence and comparability

15.1. Comparability – geographical

The regional classification (municipalities, counties, welfare regions) in force in each statistical year is used in the statistics.

15.2. Comparability – over time

The statistics have been compiled since 1981. From the beginning, they have reflected the number and average pensions of persons receiving a pension from the earnings-related and/or national pension schemes. During this period, several legislative changes have been made to both pension schemes, and the coverage of the statistics has been extended over the years. However, the time series of the statistic are broadly comparable.

The comparability of the time series is affected by the following changes:

In 1991 the statistic were completed by adding the money amounts of SOLITA pension to the pensions of persons receiving an earnings-related and/or national pension. SOLITA pensions are included in the average pensions and in the pension size distributions. They take precedence over earnings-related and national pensions, so that this additino is an essential complement to the pension coverage of these persons.

In 1996, a new concept of ‘own pension’ was introduced in the statistics, replacing the previous concept of ‘own and/or special pension’.

From the beginning of 2001, the basic component of the national pension was no longer paid. This change did not affect the total number of pensioners, but it shifted the number of recipients of both earnings-related and national pensions towards those receiving only earnings-related pensions. The abolition of the basic component was due to the transformation of the national pension into a reduced earnings-related pension at the beginning of 1996, when the national pension was no longer granted without a supplementary component. Before 1 January 1996, national pensions without a supplementary component were gradually reduced over a period of five years. With the abolition of the basic component, from 1996 onwards, a national pension paid solely as a pensioner’s housing or care allowance, child allowance or front-line allowance is not counted as a national pension for the purposes of these statistics.

Since 2008, the concept of national pension changed and the housing or care allowance of a pensioner is no longer counted among pensions. They are thus not included in the figures of this statistic or in the pension figures in the other statistics of Kela. The change slightly reduced average pensions.

Since 2011, when the Guarantee Pension Act came into force, the cash amount of the guarantee pension was added to the total pension of pensioners receiving earnings-related and/or national pension (not to pension in one’s own right or survivors’ pension.) The change raised the averages of total pensions.

As of the statistical year 2020, survivors’ pensions (the surviving spouse’s pension and orphan’s pension) that amount to 0 euro are no longer included in figures of the statistics. This change affects the number of recipients of survivors’ pensions and the average pension level.

The amount of the paid survivors’ pensions is affected by the surviving spouse’s own earnings-related pension (or calculated accrued pension) and benefits paid based on motor liability and accident insurance. Taking them into consideration may lead to a survivors’ pension of 0 euro.

15.3. Coherence – cross domain

Differences in definitions make comparisons with other statistics for the same statistical domain difficult.

These statistics cover only statutory pensions, excluding, for example, voluntary supplementary pension schemes.

15.4. Coherence – internal

The data on earnings-related pensions in this statistics correspond to the data in the statistics Earnings-related Pension Recipients in Finland, published by the Finnish Centre for Pensions.

Earnings-related Pension Recipients in Finland

The data on national pensions differ from the Kela pension statistics with regard to the concept of ‘new retiree’. The Kela statistics use the term ‘new pensions’.

16. Cost and burden

The production of the statistics is financed jointly by the Finnish Centre for Pensions and Kela.

17. Data Revision

–

18. Statistical processing

18.1. Source data

The statistics is based on the registers of the Finnish Centre for Pensions and Kela.

18.2. Frequency of data collection

–

18.3. Data collection

Administrative registers.

18.4. Data validation

Adjustments are made at different stages of statistical production in accordance with the production processes of the Finnish Centre for Pensions. In addition, the results are compared with changes in legislation and with data from previous statistical years.

18.5. Data compilation

Combination of person-level pension data extracted from the registers of the Finnish Centre for Pensions and Kela. Further processing produces aggregated data and statistical tables.

Description of the pension system in 2023

The Finnish statutory pension system consists of the statutory earnings-related pension, the national pension and the guarantee pension. In addition to these, pensions are paid based on the Motor Liability Insurance Act, the Workers’ Compensation Act, the Act on Compensation for Military Accidents and Service-Related Illnesses and the Act on Compensation for Accidents and Service-Related Illnesses in Crisis Management Duties.

The earnings-related pension scheme covers all employees, self-employed persons and farmers whose employment exceeds the minimum requirements laid down by law.

The national pension and the guarantee pension secure a basic livelihood if the retiree has accrued no or only a small earnings-related pension. The national pension scheme covers all persons who are permanently residing in Finland.

Earnings-related pension scheme

Pension accrues for work carried out between the ages of 17 and 67. For the self-employed, pension accrues as of age 18. The pension is calculated based on the person’s earnings for each year and an age-specific accrual rate. Pension also accrues based on certain unsalaried periods, such as periods of unemployment or study. A person can simultaneously receive earnings-related pensions under several pension acts and of several different types.

The Ministry of Social Affairs and Health annually confirms the earnings-related pension index and the wage coefficient. The earnings-related pension index is used to revalue the euro amounts of pensions in payment at the beginning of January each year. The wage coefficient has been used as of 2005 to calculate pensions and to revalue earnings from work, self-employed persons’ confirmed income and the limit amounts laid down in the acts on the earnings-related pension. In 2023 the earnings-related pension index was 2874 and the wage coefficient 1,558.

The national pension scheme

Pension financing

The financing of private sector earnings-related pensions is based on insurance. The financing is partly funded and partly pay-as-you-go. The expenditure of the scheme is thus covered through contributions and interest yields on the funds. Contributions under TyEL and MEL are paid jointly by the employer and the employee. Contributions under YEL and MYEL are paid in their entirety by the self-employed. The State participates in the financing of the pensions for self-employed persons insofar as the contributions and interest yield on the funds are not sufficient to finance the pensions.

Until the 1990s, the financing of public sector pensions was based on the pay-as-you-go system. In other words, enough pension contributions or taxes were collected to finance pensions in payment. Municipal pensions are the responsibility of the member entities Since 1988, in preparation for the increasing pension expenditure, assets have been collected from the member entities into a pension liability fund. Since 1990, state pension contributions have been accumulated into the State Pension Fund. Pensions are not paid directly from the State Pension Fund but from the state budget. Employees and officials of the public sector also participate in the financing of pensions by paying the employee’s pension contribution.

Kela pensions are financed by the State.

Pension legislation as at 31 December 2023

Earnings-related pension acts

Private sector

- TyEL Employees Pensions Act

- MEL Act Seafarer’s Pensions Act

- YEL Self-Employed Persons’ Pensions Act

- MYEL Farmers’ Pensions Act

- LUTUL Act on Farmers’ Early Retirement Aid

Public sector

- JuEL Public Sector Pensions Act

- OrtKL Orthodox Church Act

- SP Pension regulation for the Bank of Finland

- KELA Pension regulation for Kela

- Pension regulation for the regional government of Åland

National pension acts

- KEL National Pensions Act

- REL Front-Veterans’ Pensions Act

- URL Act on Front-Veterans’ Supplement Payable Abroad

Special provision acts

The Motor Liability Insurance Act compensates personal injuries caused by motor vehicles used in traffic. Compensations are paid based on the Workers’ Compensation Act for accidents at work (on the job or on the way to and from work) or occupational diseases.

Farmers are covered by the Accident Insurance Act for Farmers. Military injuries and service-related illnesses occurring in military service, non-military service and women’s voluntary military service are compensated under the Act on Compensation for Military accidents and Service-Related Illnesses. Accidents and service-related illnesses occurring in crisis management operations are compensated under the Act on Compensation for Accidents and Service-Related Illnesses in Crisis Management Duties.

Act on Guarantee Pensions

The guarantee pension ensures a minimum pension of a certain size for a person resident in Finland. Kela pays out the guarantee pension, which is financed by State funds. The guarantee pension is adjusted annually with the national pension index.

Pension benefits in 2023

Old-age pension

In the earnings-related pension scheme, it is possible to retire on an old-age pension flexibly between the ages of 63 and 68. The retirement age rises gradually from 63 years to 65 years with 3 months per age group. The first age group whose retirement age rises are those born in 1955.

In the public sector of the earnings-related pension scheme, it is possible to retire according to earlier agreement at an individual or occupational retirement age. Under MELA, it is possible to retire at an accrued retirement age.

From the beginning of 2017, it has been possible to retire on an earnings-related partial old-age pension. This pension is available to persons born in 1949 or later who have reached the qualifying age for the benefit, determined based on year of birth. Eligible persons may not receive any other pension in their own right at the start of the partial old-age pension. The amount of partial old-age pension is 25 or 50 per cent (based on the individual’s own choice) of the earnings-related pension accrued at the time of retirement. An early retirement reduction is made to the pension if it is taken out before the retirement age of the age group concerned. There are no rules regarding employment; partial old-age pension recipients may continue to work if they want to.

In the national pension scheme, the age limit for the old-age pension is 65 years. Persons born before 1962 can take out their national old-age pension early. The age threshold is 63 years for persons born before 1958 and 64 years for persons born in 1958–1961. Early retirement reduces the pension permanently.

Retirement on old-age pension can also be deferred. The earnings-related old-age pension is increased if taken out late, after reaching the retirement age. Under the national pension scheme, the age threshold for the increase is 65 years.

Disability pension

The earnings-related disability pension may be granted to persons who have an illness which reduces their ability to work. Besides health, the person’s possibilities of earning a living (by such available work which the person can reasonably be expected to manage considering their education and training, age, previous activities, living conditions and other comparable factors) are considered. In the public sector it suffices that, due to an illness, a handicap or an injury, the person has become incapable of doing their own job. When assessing whether a 60-year-old person with a long work history is entitled to a disability pension, the occupational nature of the work inability is emphasized especially.

A pension provider may grant a disability pension to an insured person who has turned 17 but who has not reached their retirement age (determined based on the birth year) . When the person reaches their retirement age, the disability pension will turn into an old-age pension. In the national pension scheme, the disability pension may be granted to an insured person who is between 16 and 64 years old.

In the earnings-related pension scheme, it is further required that the work inability can be estimated to last for at least one year. In the national pension scheme, the pension is not awarded to persons aged 16–19 until their possibilities of rehabilitation have been investigated. In the national pension scheme, a permanently blind person and a person permanently without mobile activity is always considered incapable of work.

The disability pension may be awarded either until further notice or as a fixed-term cash rehabilitation benefit. The cash rehabilitation benefit is granted if it can be expected that the person’s ability to work can be restored at least in part through treatment or rehabilitation. The granting of a cash rehabilitation benefit always requires a treatment or rehabilitation plan.

The earnings-related disability pension may be awarded as a full pension or a partial pension. A person is granted a full disability pension if their ability to work is considered to have been reduced by at least 3/5 and a partial disability pension if their ability to work is considered to have been reduced by 2/5 – 3/5. The partial disability pension is half of the full disability pension. A disability pension paid under the national pension scheme is not granted as a partial pension.

In the earnings-related pension scheme, the disability pension can also be granted as a years-of-service pension if the pension applicant has done work that requires great mental or physical effort for at least 38 years. In addition, the applicant’s ability to work must be reduced, but less so than for the actual disability pension. The first years-of-service pensions were paid out in 2018.

Part-time pension

Part-time pensions were granted within the earnings-related pension scheme in 1987–2016 to workers who changed from full-time to part-time work.

Survivors’ pension

After the death of the insured, the survivors’ pension may be paid to the children (orphan’s pension), the surviving spouse or a former spouse of the deceased (surviving spouse’s pension).

A child is entitled to the orphan’s pension if the child is under the age of 18 at the time of the death of the parent. In the national pension scheme, a child aged 18–20 is also entitled to an orphan’s pension if they are a full-time student or participates in vocational training (student’s pension). Children entitled to the orphan’s pension may be the deceased person’s own child, the surviving spouse’s child, the child of the surviving party to a registered relationship or an adopted child.

The surviving spouse’s pension may be granted to the surviving spouse if the spouses were married before the deceased reached the age of 65 and if the surviving spouse has or has had a child together with the deceased. If the spouses do not have a child together, the requirement is that the spouses were married before the surviving spouse reached the age of 50, the marriage had lasted for at least 5 years and that the surviving spouse had reached the age of 50 at the time of the death of the spouse. In the earnings-related pension scheme, the surviving spouse’s pension may also be granted to a surviving spouse aged less than 50, if the surviving spouse had received a disability pension continuously for at least three years before the death of the spouse. The above criteria also apply to the surviving party of a registered partnership.

In the earnings-related pension scheme, the survivors’ pension may also be granted to the deceased person’s former spouse or the divorced party to a registered partnership if the deceased person was, at the time of death, liable to pay alimony to the former spouse.

Special pensions for farmers

Special pensions for farmers are the farm-closure pension and the farmers’ early retirement aid. Farm-closure pensions were awarded from 1974 to 1992 and farmers’ early retirement aids from 1995 to 2018.

The farm-closure pension is a lifelong pension. The basic amount of early retirement aid granted after 2007 is converted to an old-age pension at the age of 63, while the supplementary component is paid until the age of 65.

Special pensions for farmers are paid within the earnings-related pension scheme only in the private sector.

Guarantee pension

The guarantee pension can be granted to a person who receives pension (old-age or disability pension, farmers’ early retirement aid or special provisions pensions) that qualifies them to receive the guarantee pension. In addition, the person’s combined pension income may not exceed the income limit for the guarantee pension. All pensions, including survivors’ and farm closure pensions, paid in Finland and from abroad affect the amount of the guarantee pension.

The guarantee pension may be granted to immigrants who have turned 65 years or disabled immigrants who are at least 16 years old. However, an immigrant is not entitled to the guarantee pension simply based on blindness or immobility. Receiving the guarantee pension requires that the person has been resident in Finland for at least 3 years since the age of 16. The guarantee pension is not paid to a person who resides abroad permanently.