Pension knowledge, trust, and financial preparedness

Knowledge of pensions helps individuals make informed decisions about their future retirement. Being aware of pensions also enables people to evaluate discussions on the topic and its funding based on facts.

Trust in pensions, their future, and how the pension system functions can affect the perception of how acceptable pensions are perceived and how one’s own financial situation in retirement is assessed.

From the perspective of the effectiveness and sustainability of the pension system, understanding and trust in pensions are important research themes.

Our research shows that:

- Most respondents rate their knowledge of pensions as poor or fairly poor. There is also significant uncertainty about the specifics of pensions.

- The pension system is generally considered reliable, but concerns have been raised about its functionality and future.

Understanding pensions

According to surveys, few people feel that they have a good understanding of pensions. While some aspects of the pension system are well understood, there are knowledge gaps in other areas.

Understanding pensions can be approached either through a perceived knowledge level or knowledge of particular details.

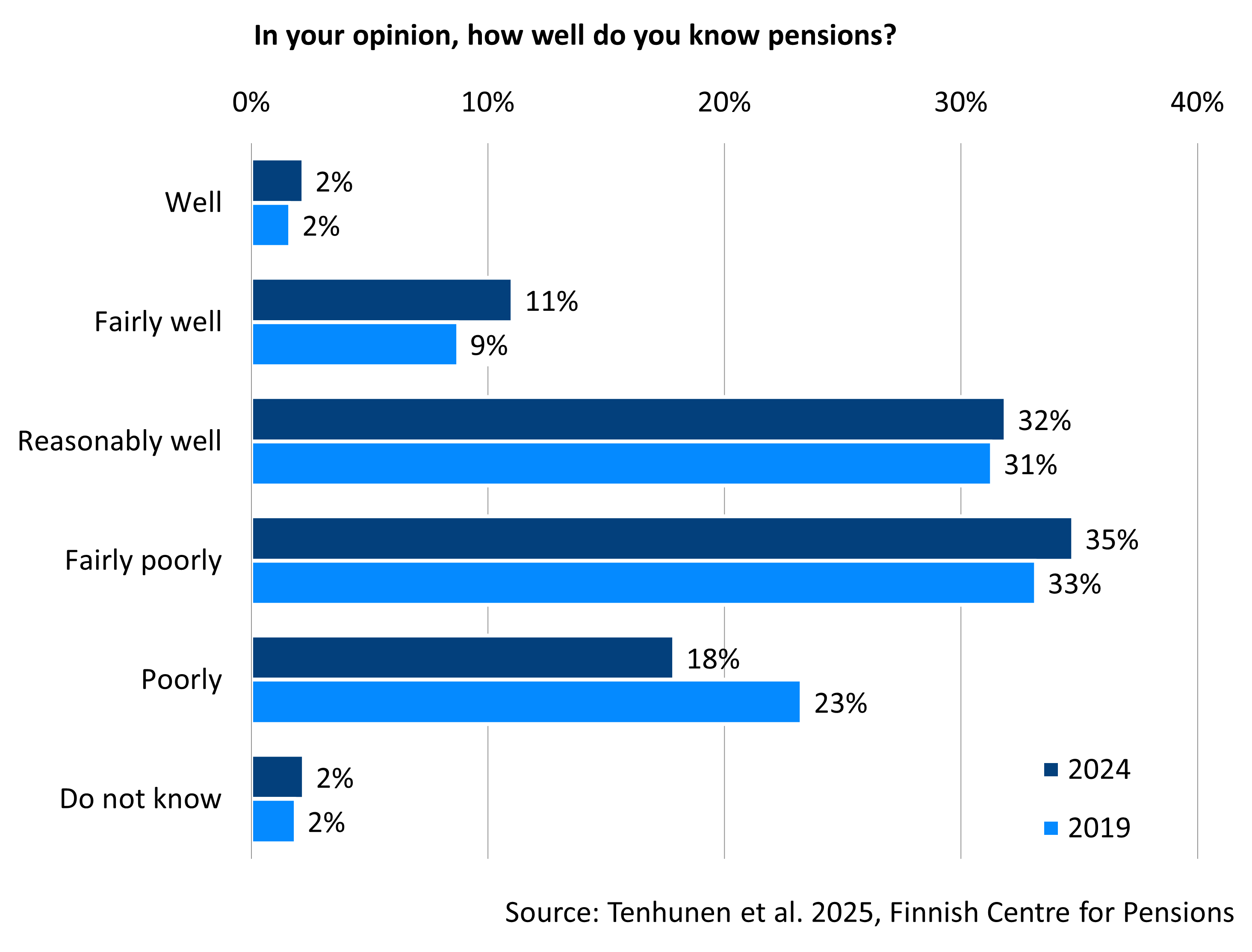

Few rate their knowledge of pensions as good

The “Views on pensions” surveys examine the pension knowledge of 25–67-year-olds. In 2024, just over half of the respondents felt that they had a poor or fairly poor understanding of pensions. Only one in eight rated their understanding as good or fairly good.

People aged over 60, those with a tertiary education, the self-employed, pensioners, and those in high-income households all rated their knowledge of pensions above average.

Graph’s “In your opinion, how well do you know pensions?” data in accessible Excel file.

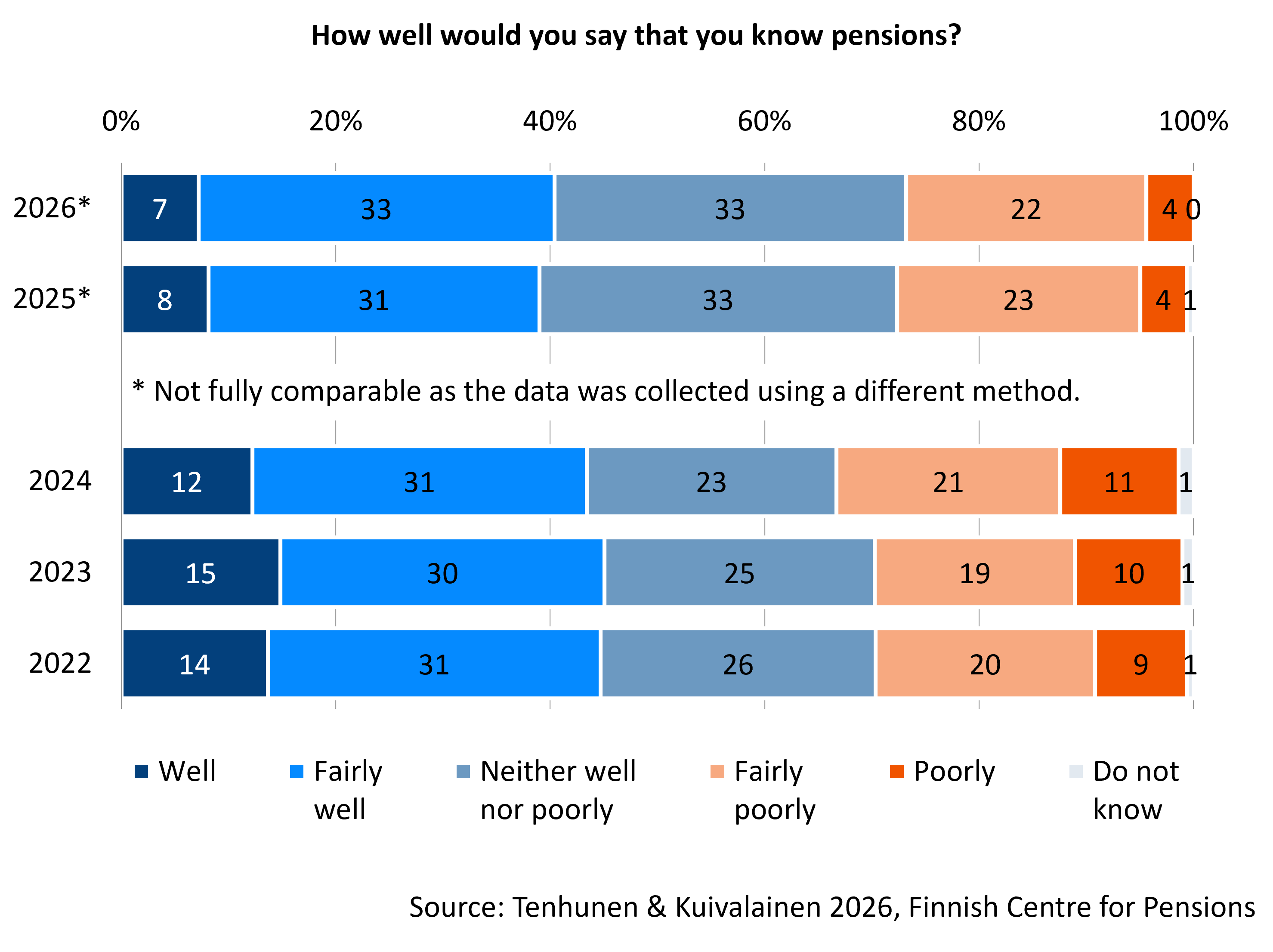

The Pension Barometer, which surveys the views of people over 18 annually, also assessed pension knowledge. Perceived pension knowledge has remained relatively stable in recent years.

In the 2026 survey, 40 per cent of the respondents rated their knowledge as good or fairly good. Men, older respondents, entrepreneurs and pensioners felt more knowledgeable about pensions. More than a quarter rated their knowledge as poor or fairly poor.

Graph’s “How well would you say that you know pensions?” data in accessible Excel file.

Publications:

- Tenhunen & Kuivalainen 2026. Eläkebarometri 2026 (Pension Barometer 2026) (Julkari)

- Tenhunen et al. 2025. Knowledge about pensions, trust in the pension system and financial preparedness: Views on pensions 2024 – Survey (Julkari)

New retirees are often aware of the increase for late retirement and the life expectancy coefficient

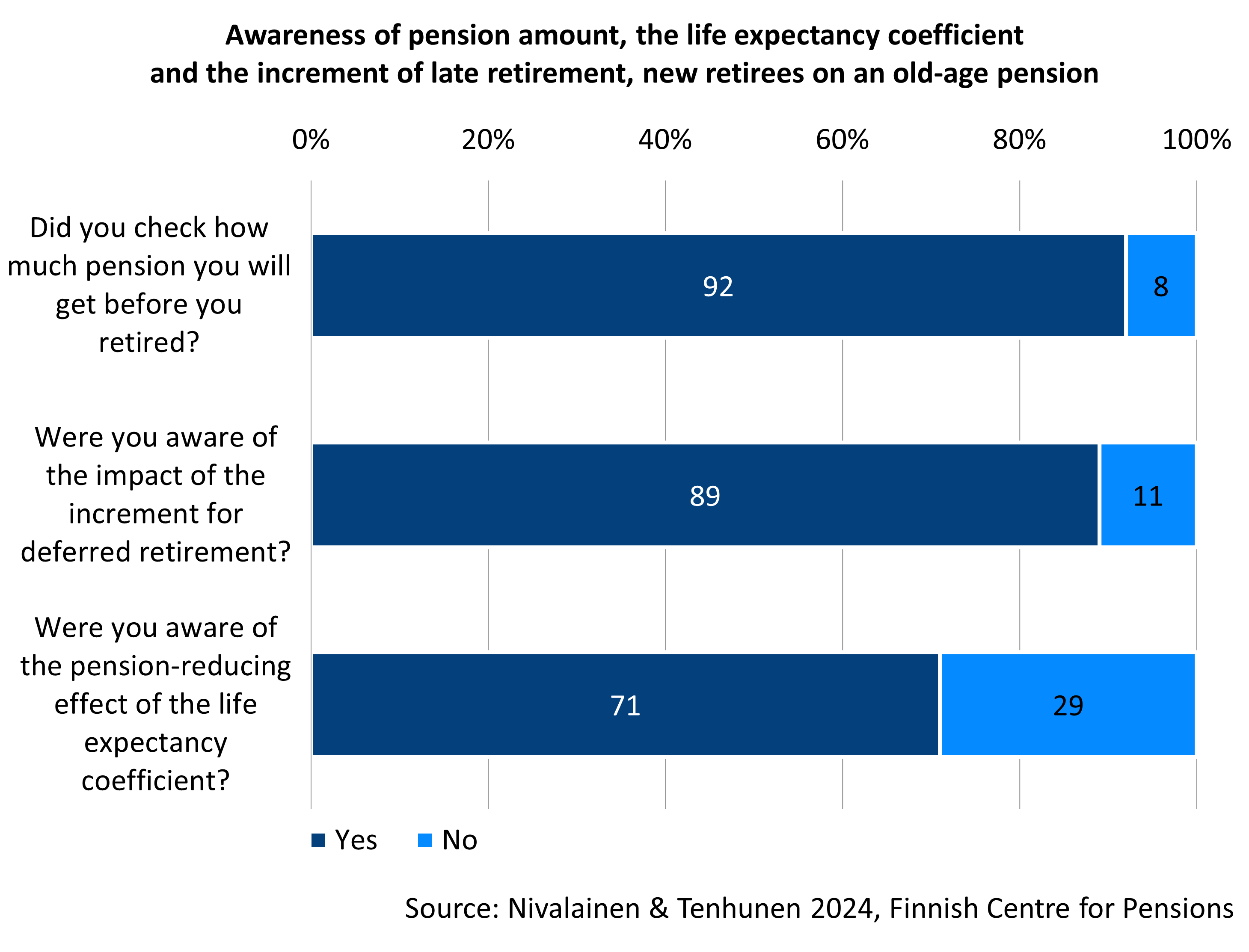

As retirement approaches, awareness of pension issues becomes increasingly relevant. At this stage, many people also check how much pension they have accrued and how the timing of their retirement will affect this amount.

A survey of people who had recently retired found that they were generally well-informed about their pension amount, as well as the effects of the increment for late retirement and the life expectancy coefficient on their pension. Around nine in ten respondents said they had checked the size of their pension before retiring. Almost the same proportion were aware of the impact of the increment for deferred retirement. Respondents with a higher level of education were more aware of these matters than those with a lower level of education.

The life expectancy coefficient, which has been in place since 2005, reduces monthly pensions in line with increasing life expectancy. Seven out of ten pensioners who had recently retired from work said that they were aware of the coefficient and its impact on their pension. Men reported being aware of the coefficient’s impact slightly more often than women.

Publications:

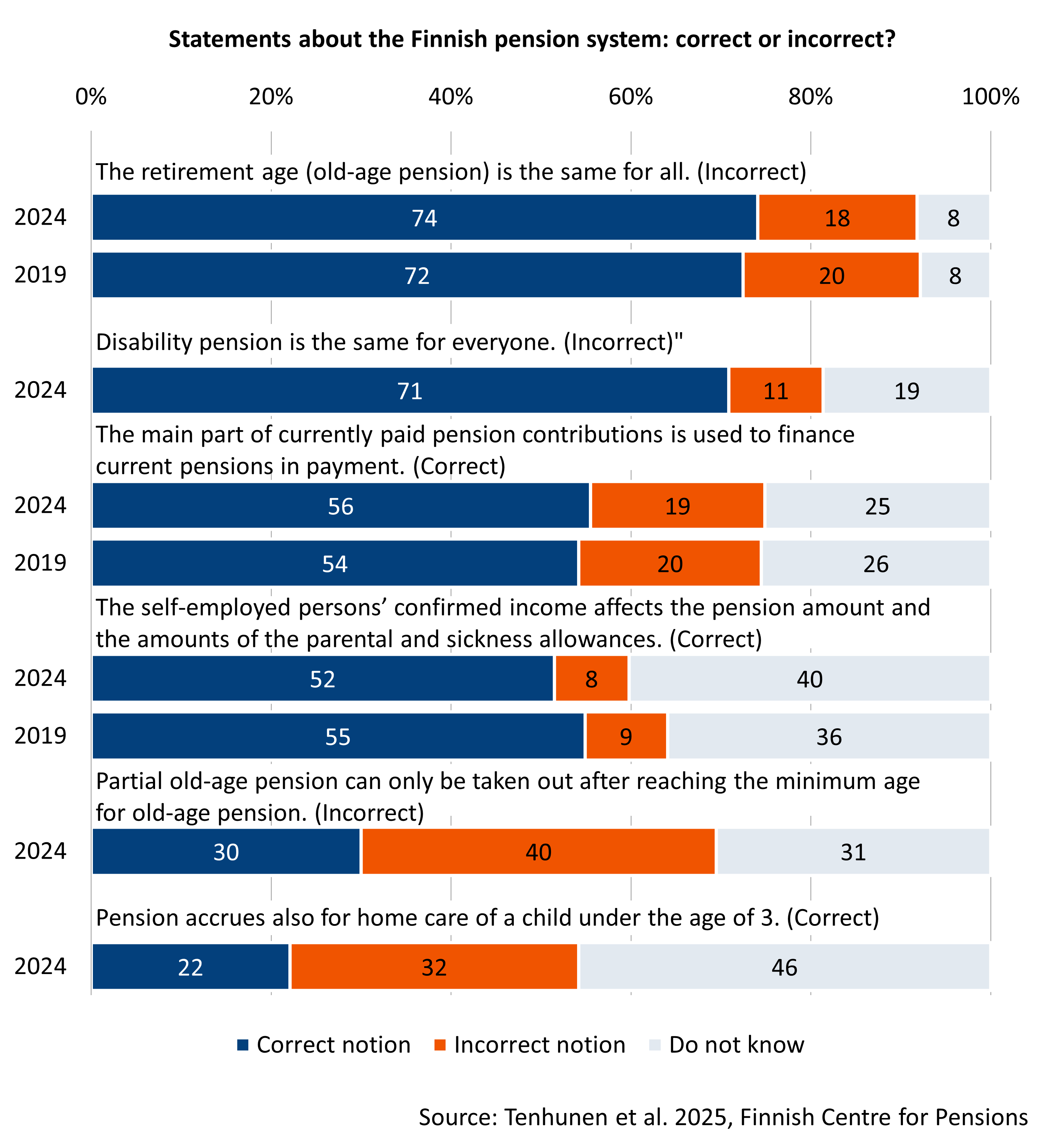

Surveys have been conducted to map the knowledge of the details of the pension system. Finns are aware that the retirement age varies and that a lion’s share of pension contributions is used to finance current pensions. However, few people know the exact amount of pension contributions deducted from wages.

Features of the pension system are understood to varying degrees

The “Views on pensions” survey mapped the pension knowledge of Finns aged 25–67 by presenting them with statements about the details of the pension system.

The facts that the retirement age for the old-age pension varies and that the amount of the disability pension is not constant were the best known.

Three out of four 25–67-year-old Finns were aware that the retirement age is not the same for everyone, varying by birth year, and that, like old-age pensions, disability pensions are earnings-related. More than half were aware that most pension contributions are used to pay current pensioners and that the earned income of self-employed individuals affects not only their pension but also certain social benefits. However, there was more uncertainty regarding the retirement age for the partial old-age pension and whether pension accrues for caring for children at home or for studying.

Similar questions were used in the Pension Barometer to assess people’s knowledge of pensions. The statement that all residents of Finland have the right to a minimum pension and that the retirement age varies according to year of birth was the most widely recognised. Most people were also aware that pension contributions are used to support current pensioners and that delaying retirement increases one’s pension. However, many were unsure about these issues.

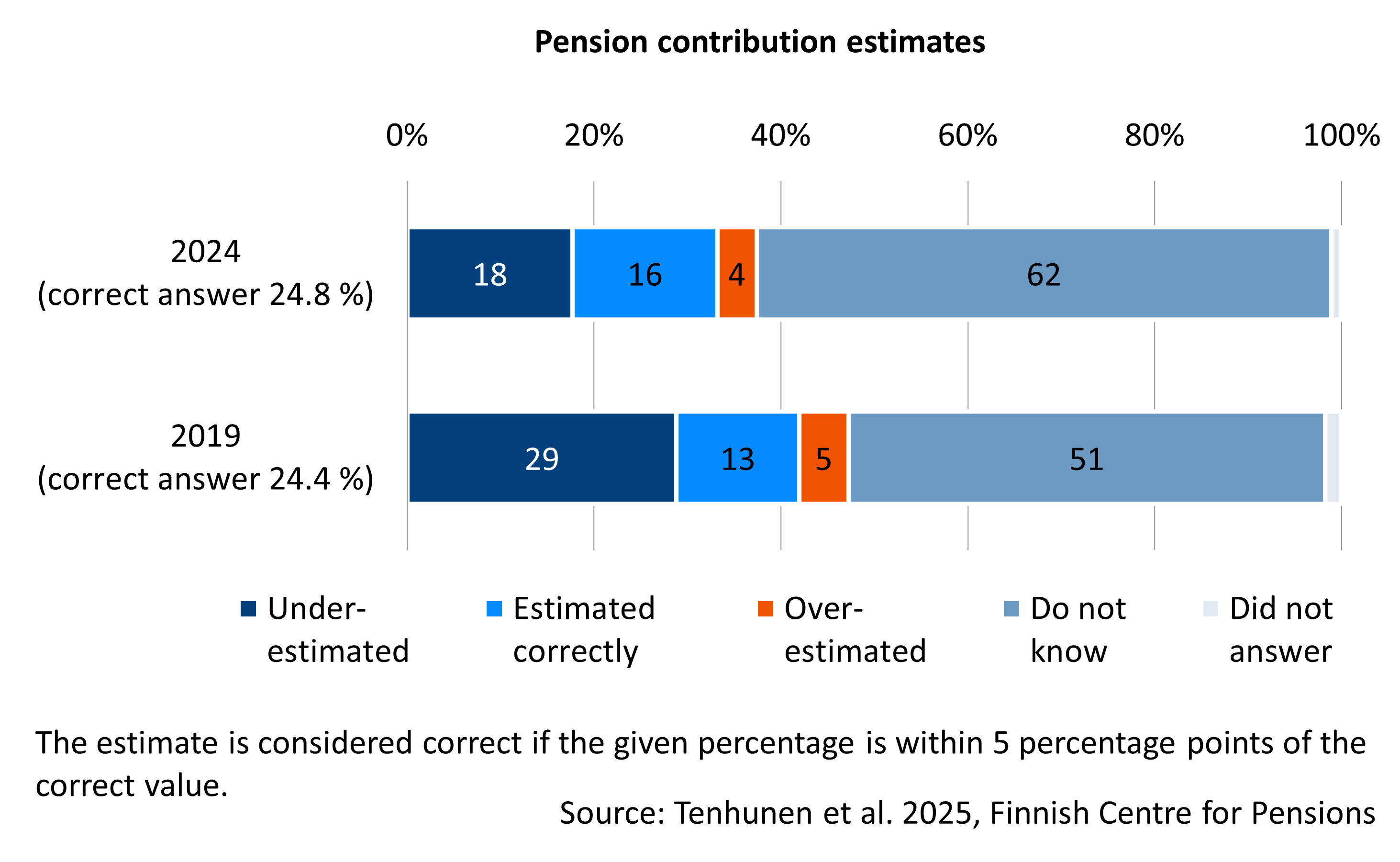

One in six working-age Finns could estimate the pension contribution rate

In the 2024 “Views on pensions” survey, respondents were asked to estimate the percentage of wages that employees and employers pay, or the percentage that the self-employed pay towards pensions. More than 60 per cent chose ‘Do not know’. Only 16 per cent of all respondents could accurately estimate the pension contribution rate within +/- 5 percentage points (range 19.8–29.8%).

Graph’s “Pension contribution estimates” data in accessible Excel file.

People with higher education qualifications and those who were self-employed were more likely to know the correct contribution rate. In contrast, those with a basic education, the unemployed, pensioners and those in low-income households were more likely to abstain from making an estimate.

Publications:

- Tenhunen et.al. 2020. How familiar are Finns with pension issues and the 2017 pension reform in Finland? Questionnaire survey on views relating to pensions (Julkari, summary in English)

- Tenhunen et al. 2025. Knowledge about pensions, trust in the pension system and financial preparedness: Views on pensions 2024 – Survey (Julkari)

- Tenhunen & Kuivalainen 2026. Eläkebarometri 2026 (Pension Barometer 2026) (Julkari)

Read more on Etk.fi:

Trust in pensions

Trust in pensions is a multifaceted phenomenon. It can be evaluated based on the system’s overall reliability, how well it fulfils its objectives, and concerns relating to pension adequacy.

Pension system generally considered reliable

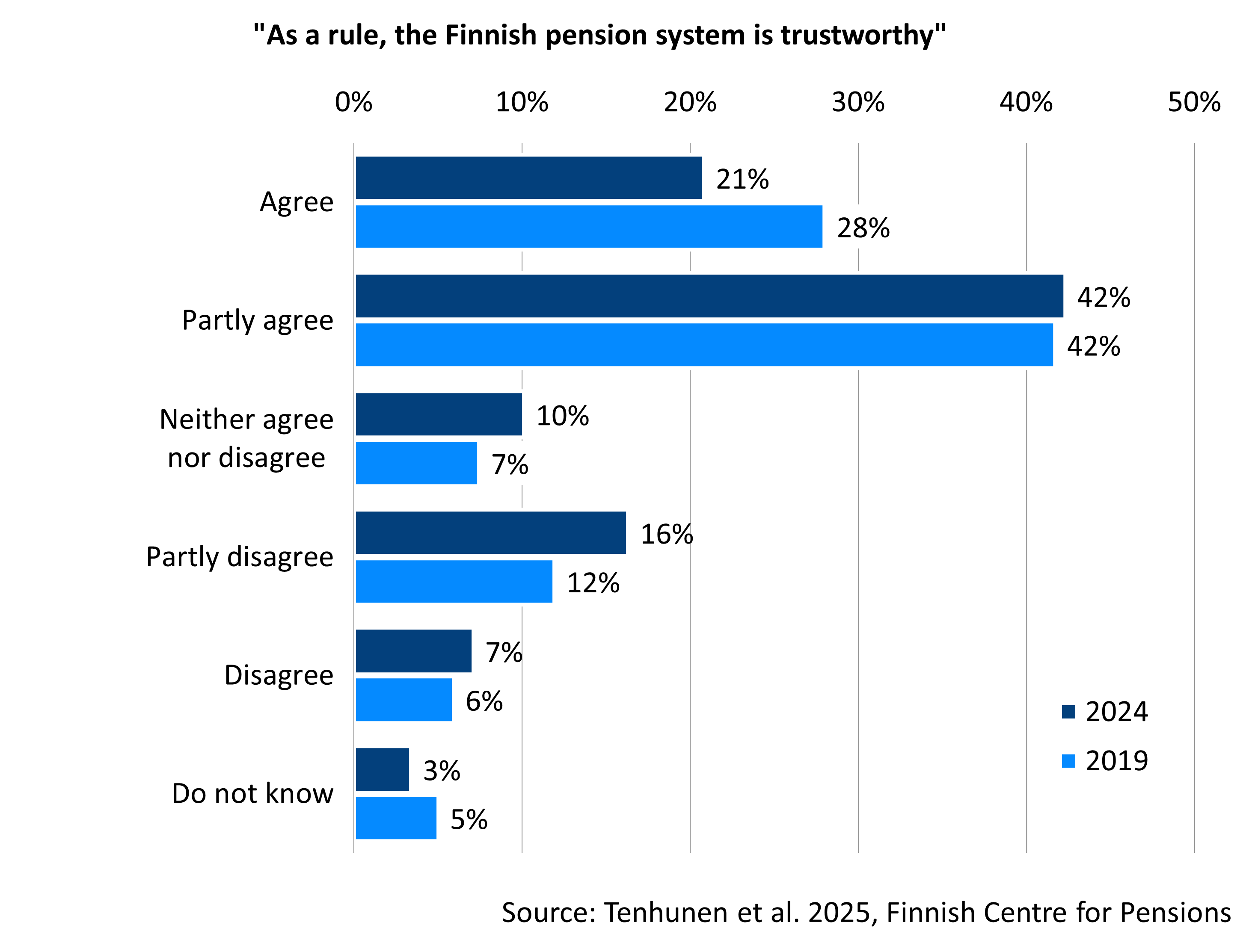

In the 2024 “Views on pensions” survey, nearly two-thirds of Finns aged 25–67 considered the Finnish pension system to be reliable. This figure is seven percentage points lower than in the 2019 survey.

The system was considered trustworthy by older respondents, pensioners and those in high-income households than by others. By contrast, people under 45, the self-employed, and those in low-income households were more critical.

Graph’s “As a rule, the Finnish pension system is trustworthy” data in accessible Excel file.

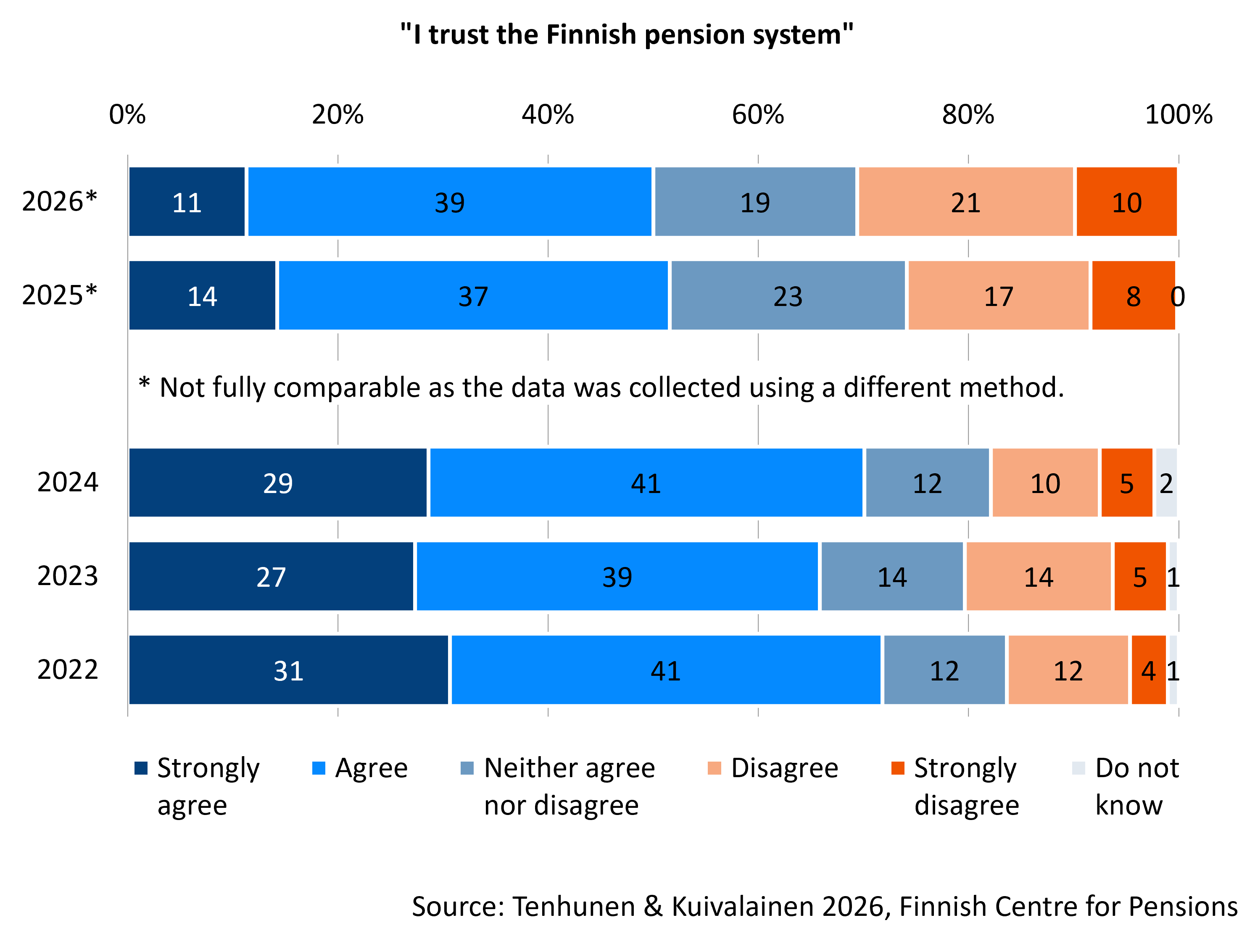

The annual Pension Barometer has also examined trust in the system. According to the survey, half of people aged 18 and over had a positive view of the pension system’s reliability. Older respondents were more likely to trust the system.

Trust in pensions in the 2026 survey was at the same level as in 2025. The figures are not fully comparable with previous years, as the Pension Barometer data up to 2024 was collected using a different method.

Graph’s “I trust the Finnish pension system” data in accessible Excel file.

Trust is affected by perceived continuity and inequality

Based on open-ended survey responses, it is evident that people’s trust in pensions is influenced by various factors. The first factor is the reliability of the system; the second is the adequacy and fairness of pensions; and the third are factors outside the system.

Factors that appear to increase trust include experiences of stability and continuity within the system, openness, access to sufficient information, and general trust in Finnish society and institutions.

Those that reduce trust include perceptions of unequal or insufficient pension levels, an ageing population and uncertainty surrounding the economic situation and political decision-making processes.

Publications:

- Liukko 2016. Mikä lisää ja mikä vähentää luottamusta eläketurvaan? (What conributes to and what reduces trust in the pension system?) (Julkari)

- Liukko & Palomäki 2024. Luottamus instituutioihin ja lakisääteinen eläketurva (Trust in institutions and statutory pensions) (Julkari)

- Palomäki et al. 2021. Trust in the pension system 2019: Questionnaire survey on views relating to pensions (Julkari)

- Tenhunen & Kuivalainen 2026. Eläkebarometri 2026 (Pension Barometer 2026) (Julkari)

- Tenhunen et al. 2025. Knowledge about pensions, trust in the pension system and financial preparedness: Views on pensions 2024 – Survey (Julkari)

The 2019 and 2024 “Views on pensions” surveys assessed people’s views on the current state and future of the pension system.

Opinions on the current state of the pension system vary

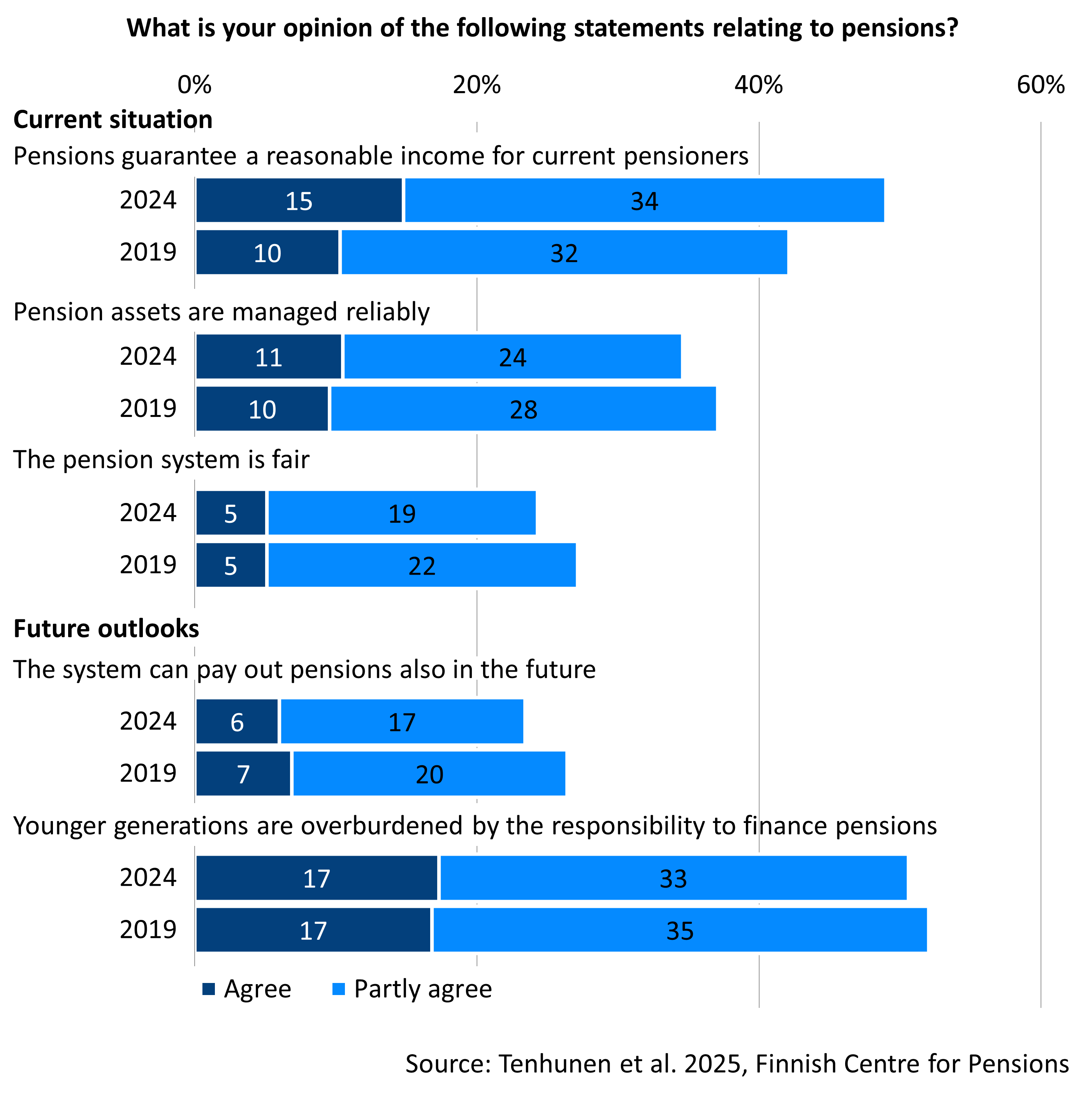

Around half of the respondents in 2024 believed that pensions ensure an adequate standard of living for current pensioners. A third were critical of their adequacy. Compared to the 2019 survey, there was an increase in positive responses and a decrease in critical responses.

Just over one-third of the respondents were positive about the reliability of pension fund management. Slightly fewer were critical, and in the 2024 survey, one-fifth disagreed or partly disagreed with the statement regarding the reliability of pension fund management.

As before, around a quarter of people thought that the pension system was fair, while nearly half disagreed.

People with higher incomes and a tertiary education were more likely to consider pensions sufficient, pension fund management reliable and the pension system fair than were those with lower incomes or lower levels of education. Older respondents were more critical of the income guaranteed by pensions, but more positive about the management of pension funds and the fairness of the system. Pensioners were more likely to consider the system fair and trust pension fund management.

Trust in the future of the pension system is lower than trust in its current state

Fewer than a quarter of the respondents believed that pensions would be payable in the future, and half considered the contribution burden on young people to be excessive.

Women and people under 45 were particularly critical of the system’s ability to pay future pensions. Young people, individuals with a tertiary education and those in high-income households were the most concerned about the contribution burden on young people.

Publications:

Several questions relating to subsistence, decision-making and economic development are associated with the way the pension system works. Trust in pensions can also be examined in relation to these issues.

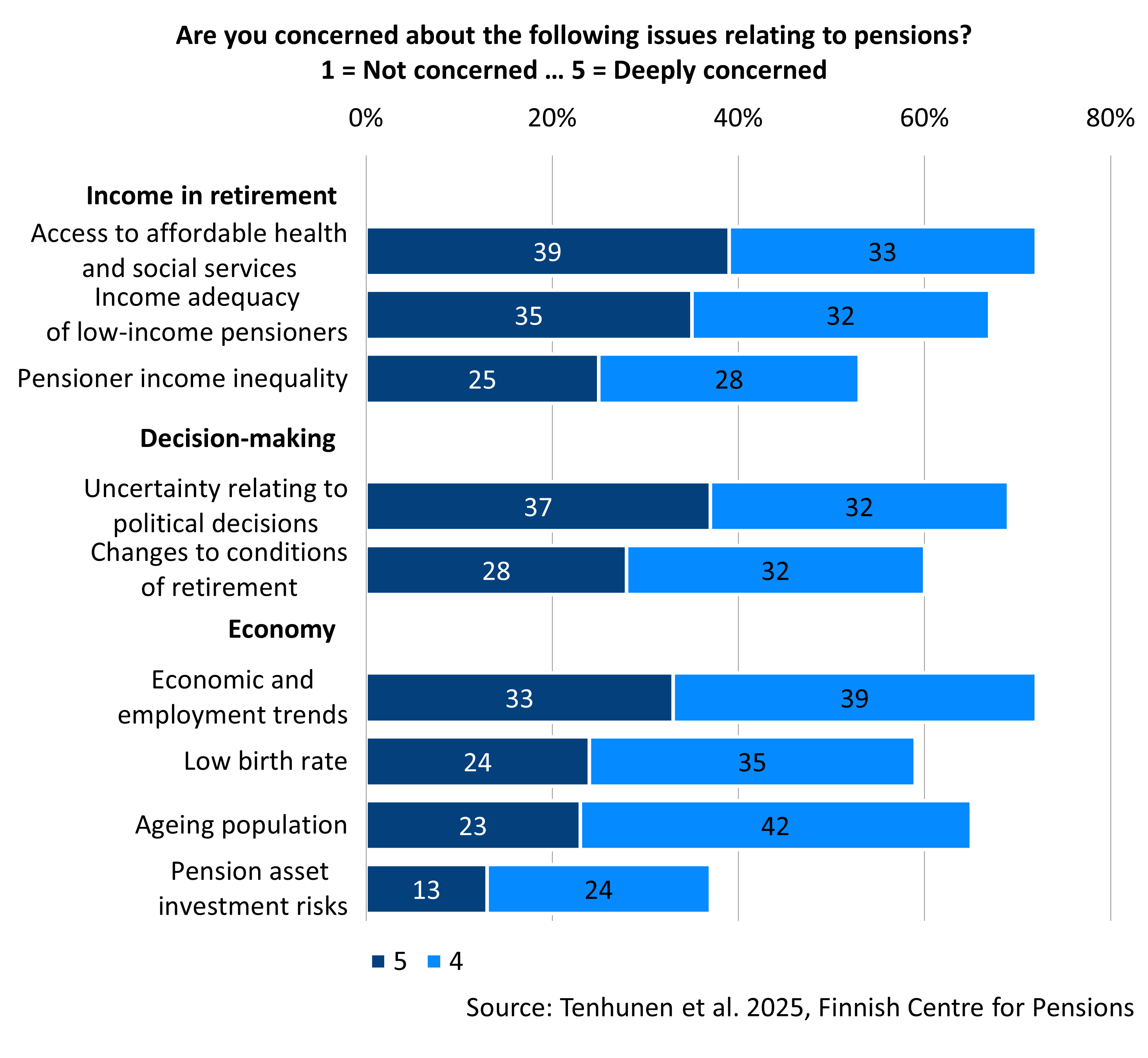

Topical issues are reflected in the things people are concerned about

The greatest concerns were the availability of affordable social and health services, the state of the economy and employment, and the uncertainty surrounding political decisions. Three out of four respondents to the 2024 survey were at least somewhat concerned about these issues. Around two out of three were worried about income adequacy for low-income pensioners and population ageing. Risks relating to pension asset investments caused the least concern.

The concerns reflected current events and issues that were widely discussed in the media at the time the survey was carried out. The main concern in the 2019 survey was the adequacy of income for low-income pensioners. By 2024, extensive public debate had taken place about pending pension reforms, challenges in social and health services, and slow economic growth and rising unemployment in Finland and around the world.

Publications:

Financial preparedness for retirement

The pension system aims to provide everyone with a basic income and a reasonable standard of living in retirement. In addition, it is possible to supplement this income by saving for retirement.

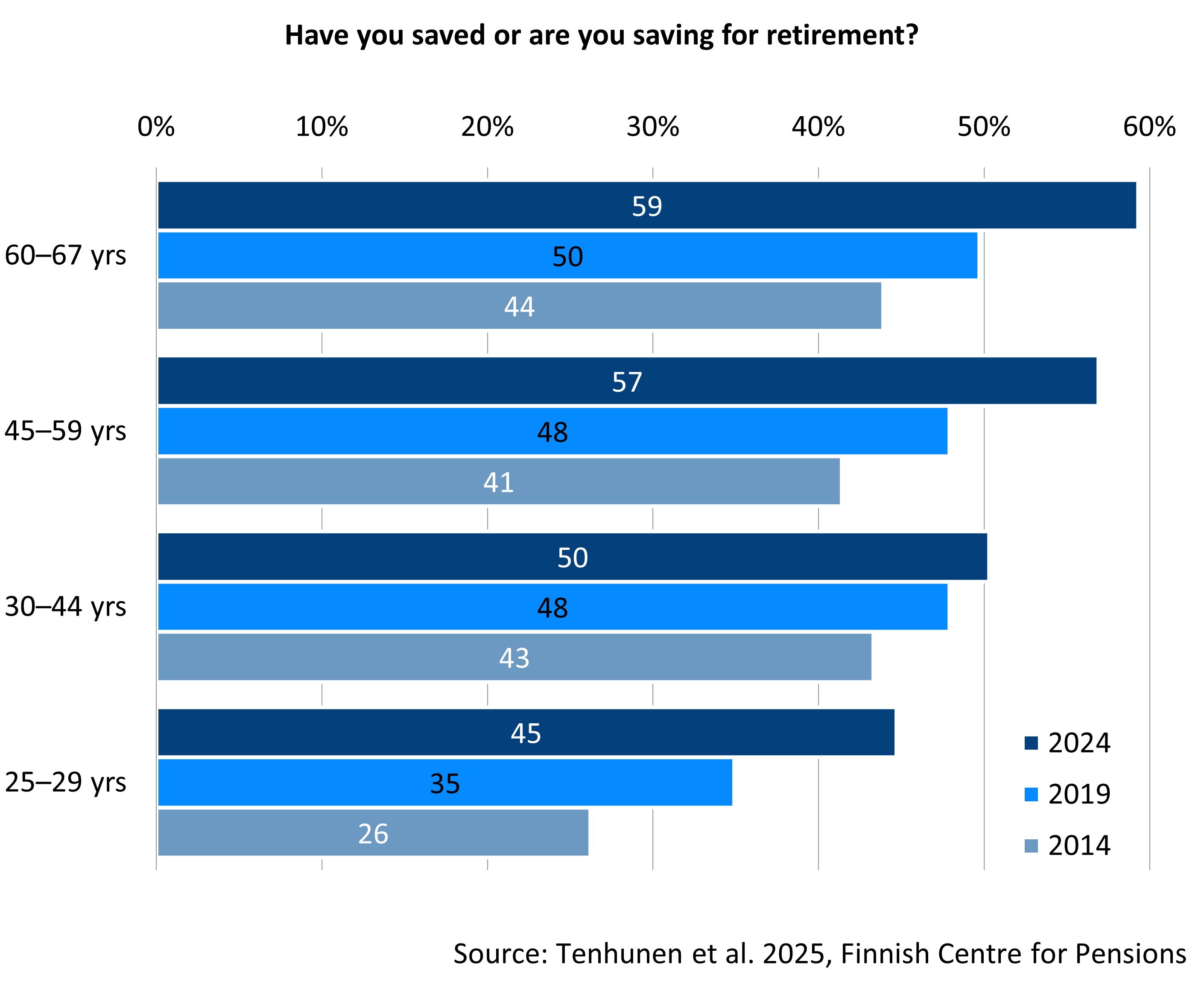

More than half of people save privately for retirement

According to surveys, the proportion of Finns aged 25–67 who save for retirement has increased. In 2024, 54 per cent of working-age Finns reported having done so. This figure was 40 per cent in 2014. Of those saving for retirement, more than half said they save regularly each month.

Financial preparedness for retirement increases with age. Saving has become more common in all age groups over the past decade. Nearly half of young people also reported saving for retirement.

The most common reason for not saving for retirement was financial circumstances. Almost two out of three cited lack of financial means as the reason.

Graph’s “Have you saved or are you saving for retirement?” data in accessible Excel file.

The importance and uses of savings can vary

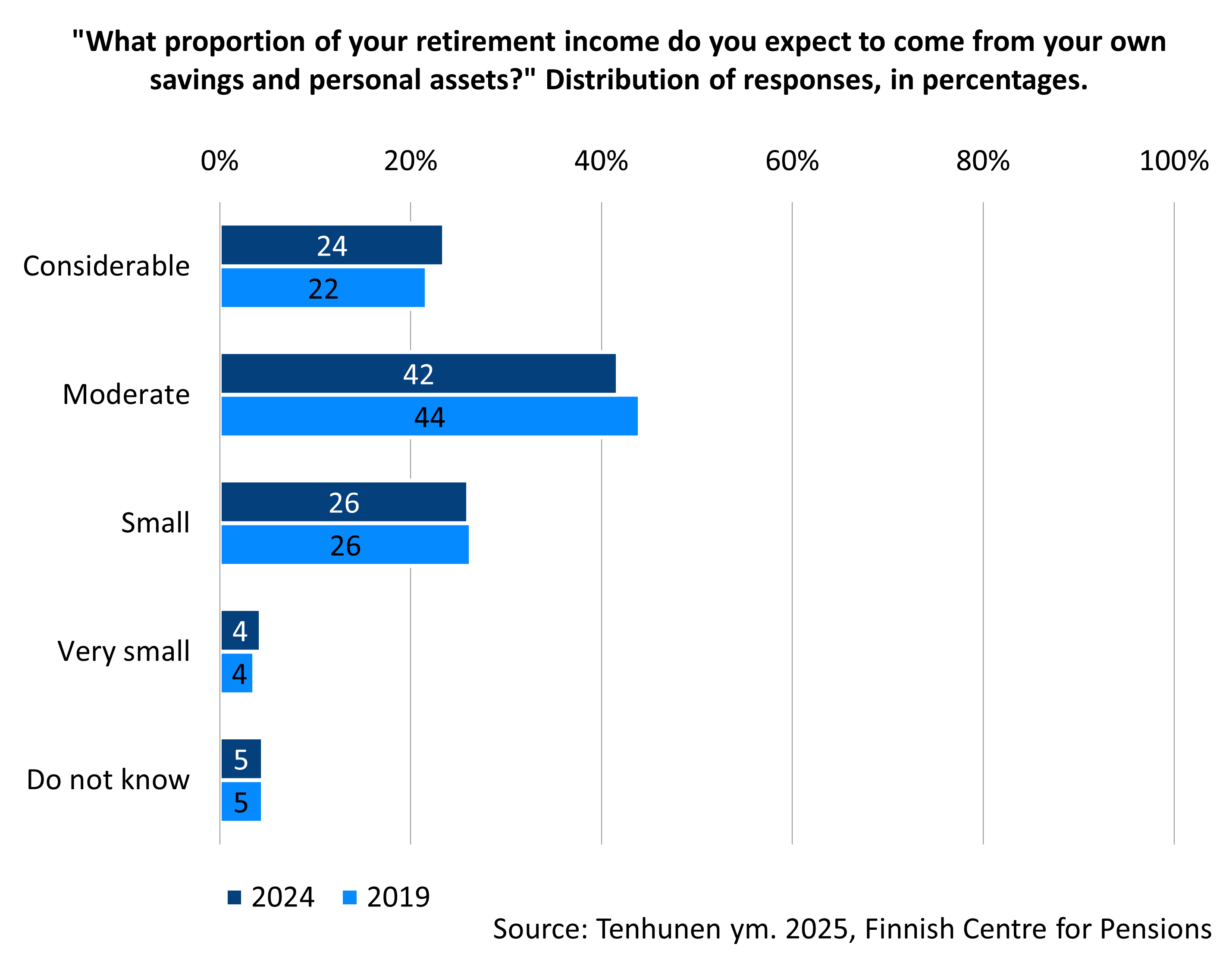

A quarter of people who had saved for retirement estimated that their savings and assets would account for a significant proportion of their retirement income. An equal proportion considered the role of their savings to be minor. Respondents under 45 were more likely than older respondents to consider their savings to be important for their retirement income.

Historically, savings were intended primarily to cover everyday expenses in retirement. However, over the past decade, the ways in which savings are used have diversified.

The most frequently mentioned uses were daily living expenses, unexpected costs, and care and nursing services. Many people also mentioned using their savings for hobbies and holidays.

Publications: