Pension Assets and Contributions

International comparison of pension financing

As a rule, earnings-related pensions are financed through contributions paid by employers and workers. Pension assets can also be used to finance pensions. Some of the pensions are financed with general tax revenues. In Denmark, for example, a considerable part of the financing of statutory pensions comes from tax revenues.

Below is a more detailed account of pension funds and pension contribution levels in different countries.

Pension assets

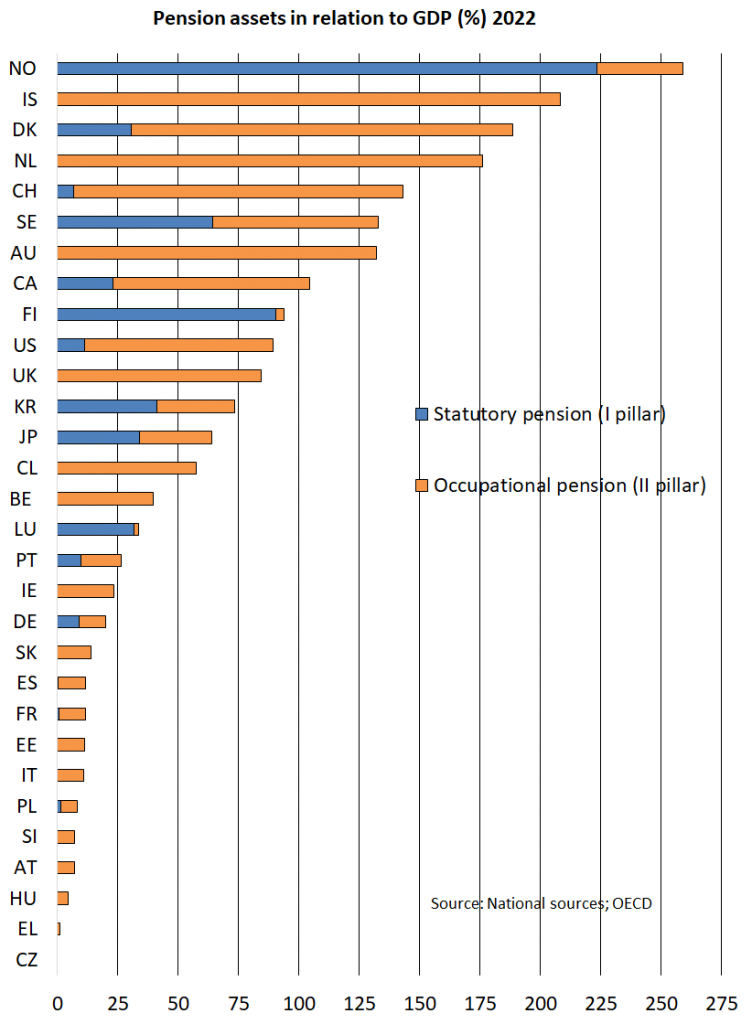

In Finland, the statutory earnings-related pension system is partly funded. For example, private sector pensions have been partly funded since the pension system came into force in 1962. Several other European countries have had equivalent buffer funds only since the 1990s and, as a rule, their statutory pension systems are based on a pay-as-you-go (PAYG) principle and lack prefunding. That is why, compared to Finland, the accumulated pension assets are comparatively smaller in these countries.

Supplementary pension schemes are usually funded. For example, the extensive pension assets of Denmark and the Netherlands are a result of comprehensive, fully funded supplementary pensions. The French mandatory supplementary pensions AGIRC and ARRCO form an exception in that they are based on the PAYG principle.

In the following comparative graph, the size of pension assets in different countries is presented relative to the country’s GDP. The statistics cover both statutory (pillar I) and labour market based supplementary pensions (pillar II), but not individual pension policies. As a rule, the comparisons are based on the data of OECD’s Global Pension Statistics which, for many countries, has been supplemented with national statistics.

For example, the figure for Norway includes not only occupational supplementary funds but also the data of the Government Pension Fund which are missing from OECD’s statistics. The extensive oil assets of Norway make the country a special case. The pension fund is largely based on the oil. Despite its name, the Government Pension Fund is not intended to cover pension expenditure only. Part of its return is used to balance the state budget.

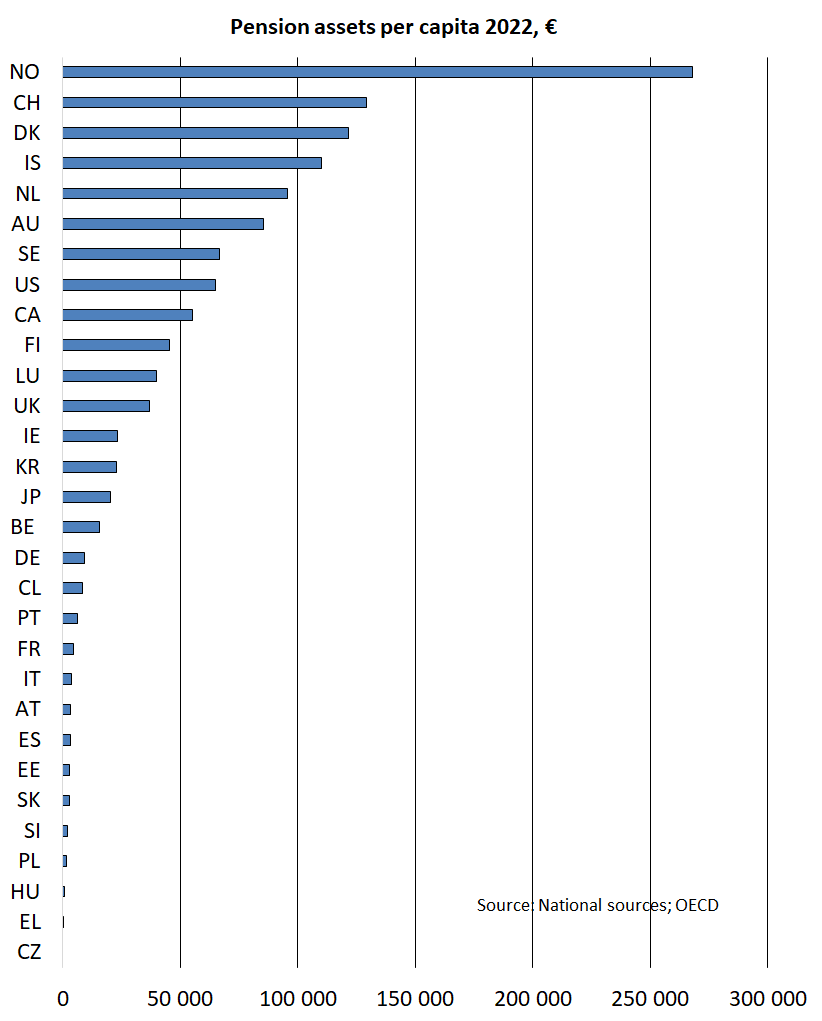

Below is a chart of the pension assets per capita in euros.

More on other sites

- The Finnish Pension Alliance TELA

- OECD: Global Pension Statistics

- SSA: Social Security Programs Throughout the World

Pension contribution comparison of the Finnish Centre for Pensions

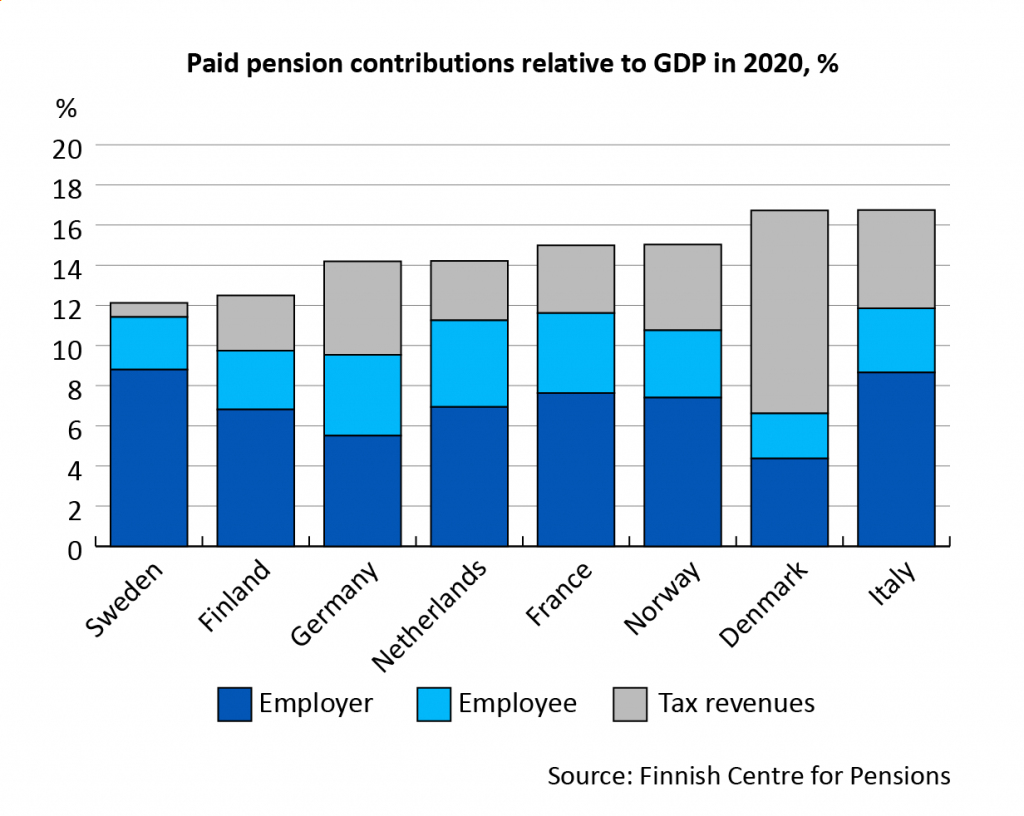

As a rule, comparisons of pension contributions and expenditure include only statutory pensions. In most European countries, however, labour market supplementary pensions form a considerable part of the total pension.

A comparison that covers only statutory pensions is problematic in particular from Finland’s point of view. Supplementary pension schemes are rare in Finland and, as the accrual of statutory earnings-related pension of wage earners is in no way limited by earnings or pension ceilings, nearly all pension contributions paid are statutory.

A more realistic and, from the point of view of the Finnish scheme, a more comparable view of the total contribution burden in different countries is achieved by reviewing the combined contribution levels of both statutory and labour market supplementary pensions.

The Finnish Centre for Pensions’ comparison of contribution levels offers a view of the overall pension contribution burden in different countries, taking into account not only statutory pension contributions but also contributions for supplementary pensions and the State’s share in pension financing.

The comparison shows that when supplementary pensions are excluded from the study, the view of the overall pension contribution burden in different countries is misleading. From the point of view of the comparison, the central result is that the countries’ contribution levels are becoming more uniform when the comparison includes not only statutory contributions but the overall contribution burden of the pension schemes.

Read more

- Cross-national comparison of pension costs reveals: Lowest contribution levels in Sweden and Finland

- Pension contribution levels and cost-sharing in statutory and occupational pensions : a cross-national study of eight European countries

The Finnish Centre for Pensions has compared international pension contribution levels since the early 2000s. Previous publications are listed below.

- What is the cost of total pension provision and who pays the bill? – Cross-national comparison of pension contributions

- Pension Contribution Level in Nine European Countries

- Pension Contribution level in nine European Countries

- Pension Contribution Level in the United States and Canada

- Pension Contribution Level in Sweden

- Pension Contribution level in France

- Pension Contribution Level in Germany

- Pension Contribution Level in the Netherlands

- Pension Contribution Level in Switzerland

- Pension Contribution Level in Great Britain

- Pension Contribution Level in Denmark

- Pension Contribution Level in Norway

- Pension Contribution Level in Finland