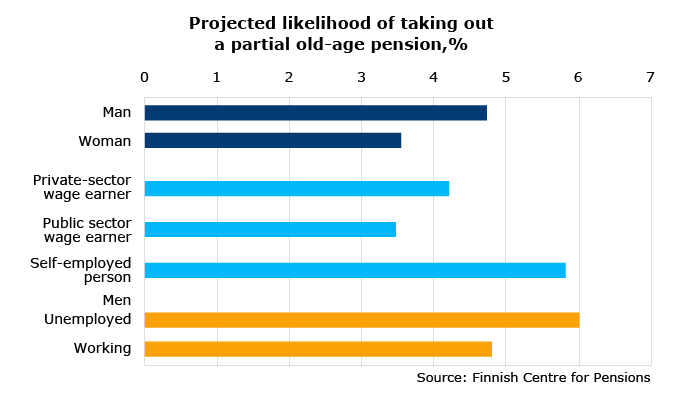

Self-employed and unemployed show most interest in new pension benefit

Urban-dwelling males aged 61 are the most likely to take a partial old-age pension. A recent study by the Finnish Centre for Pensions indicates that the self-employed and unemployed are more likely to take payment of the pension than wage earners.

The study found that by the end of June 2018, an estimated 8 per cent of all those eligible had taken a partial old-age pension. Almost all of them had taken payment of the pension early, that is, before full retirement age.

The partial old-age pension appeals most particularly to two very different groups: the self-employed and unemployed men. These groups are more likely to take their pension early than wage earners. Likewise, persons with a lower-degree tertiary education and lower-level employees are more likely to take advantage of the option of the partial old-age pension than others.

“Among women educational background, employee status or unemployment have no bearing on the decision to take early payment of their old-age pension. Self-employed women, on the other hand, are just as interested in taking the pension as men,” says Finnish Centre for Pensions’ economist Satu Nivalainen.

Many who choose an early pension continue working

The partial old-age pension is most commonly take at age 61. Over 70 per cent of those who decide to take early payment of their pension start at this age.

Most people who were employed at the time they started to take their partial old-age pension have remained at work.

Men decide to take early payment of their old-age pension somewhat more often than women. Men have typically worked a long career in the private sector.

Highly educate retire late

Around one in ten partial old-age pensions start at or after full retirement age. The results of the study show that persons with a high education and high socio-economic status are over-represented among those who decide to take their pension late.

“People in a strong labour market position often remain at work longer than others. Those who take their pension late are more often women, single and live in lower unemployment regions than those who decide to take early payment,” says economist Sanna Tenhunen.

Partial old-age pension provides freedom of choice

The Finnish Centre for Pensions research team say that the partial old-age pension provides greater freedom of choice towards the end of the individual’s working life than the previous part-time pension scheme, including those who were not eligible for a part-time pension.

“Only persons in full-time employment were eligible for the part-time pension. In addition, there were rules that required shorter working hours as well as a ceiling for earnings. There are no such limitations with the new partial old-age pension. The only restriction is the age limit and, obviously, that the individual has accrued earnings-related pension,” says senior researcher Noora Järnefelt.

The research material comprises data on 230,000 persons living in Finland and born between 1949 and 1957. The data are drawn from Finnish Centre for Pensions register sources.

Partial old-age pension in a nutshell

- gives persons aged at least 61 the opportunity to take payment of one-quarter (25%) or half (50%) of their accrued pension funds,

- is adjusted with the life expectancy coefficient,

- is permanently reduced by 0.4%for each month of early retirement,

- is permanently increased by 0.4%for each month of late retirement, and

- includes no restrictions on working hours or earnings and no rules regarding employment status.

Publication:

Who opt for a partial old-age pension? A study on the factors behind the choice to take early payment of a partial old-age pension, Finnish Centre for Pensions, Studies 06/2018

More information

Satu Nivalainen, Economist, phone +358 29 411 2151, satu.nivalainen(at)etk.fi

Sanna Tenhunen, Economist, phone +358 29 411 2492, sanna.tenhunen(at)etk.fi

More information on the partial old-age pension and how to apply for it (Työeläke.fi)

Photo: Gettyimages