Long-term projections: Pension financing relies increasingly on investment returns

The long-term pension financing outlook has improved considerably due to favourable investment returns. At the same time, uncertainty about future contribution rates has grown. If the birth rate remains low, an increasing share of rising pension expenditure will have to be covered by returns on pension assets.

The long-term projections of the Finnish Centre for Pensions take into account the mortality rates, inflation and investment returns until the end of July 2022.

The projections are based on Statistics Finland’s population forecast from 2021. According to the forecast, birth rates will remain low and the working-age population will decline throughout the projection period (2021–2090). At the same time, the old-age dependency ratio will nearly double.

In recent years, earnings-related pension assets have yielded a better-than-expected return. According to the projection, pension assets under the Employees Pensions Act (153 billion euros in 2022, in 2021 prices) will grow and accumulate in the long-term and cover an increasingly larger share of pension expenditure.

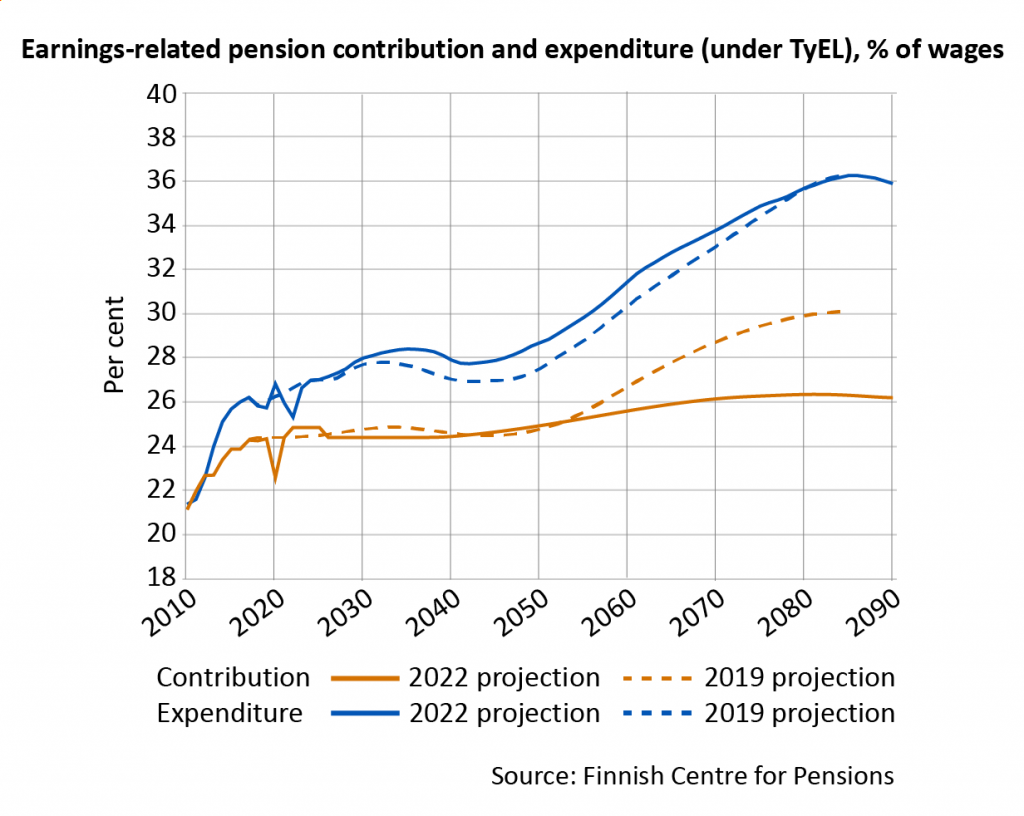

The private-sector insurance contribution under the Employees Pensions Act (TyEL contribution) can be kept below 25 per cent of wages until the 2050s. Long term, the pressure to increase the contribution rate persists but has declined by four percentage points since our previous (2019) projection.

The TyEL contribution rate can be kept at a level of 26 per cent of wages at the end of the century if the real return on pension assets is at least 3.5 per cent over the long run.

“We mustn’t stop improving the earnings-related pension system because the improved financial position due to good investment returns masks significant vulnerabilities such as low birth rates”, says Director Allan Paldanius (Finnish Centre for Pensions).

If the earnings-related pension system is viewed as a whole, there is no upward pressure on pension contributions. On the contrary, there is even some room to lower contributions. In 2021, the total contribution level of the earnings-related pension scheme was 29 per cent of the economy’s sum of earned income. The current contribution level could be reduced by one percentage point, which would be sufficient also in the future.

Contribution greatly affected by investment returns

During the next ten years, the real return on pension assets is expected to be 2.5 per cent, after which it is assumed to rise to 3.5 per cent.

When an increasing share of pension expenditure is covered by pension assets, investment returns become an increasingly significant factor in pension financing.

A return that is slightly over one percentage point higher or lower than in the baseline projection would impact the earnings-related pension contribution level by nearly one and a half percentage points in 2040.

In the long run (2090), a slightly over one percentage point higher return would allow for a TyEL contribution that is nearly 10 percentage points lower than the baseline projection’s 26 per cent. In the low-return projection, on the other hand, the contribution should be raised by six percentage points to around 32 per cent.

“Tolerating uncertain returns is an integral part of investing. However, the pension system is well prepared for that because of the long-term nature of investing”, says Senior Mathematician Kaarlo Reipas (Finnish Centre for Pensions).

Pensions grow faster than wages in the next few years

In 2021, the average monthly pension in Finland was 1,784 euros. According to the projection, the purchasing power of pensions will continue to grow. For example, in 2030, the average pension is projected to be around 1,900 euros in 2021 prices.

Average pensions in payment are around 50 per cent of the average wage. In the next few years, pensions will grow even faster than earnings since prices will grow more than wages.

The ratio of the average pension to the average wage will take a downward turn in the mid-2020s. The main reason for the declining ratio is the life expectancy coefficient, which adapts the benefit level to correspond to changes in life expectancy.

Read more:

Long-term projections (Etk.fi)

Skeneraattori scenario generation application for combining sensitivity analyses (in Finnish)

The report also includes:

- optimistic and pessimistic economic growth scenarios;

- sensitivity analyses: mortality, birth rate, incidence rate of disability pensions, earnings growth, employment rate and return on pension assets;

- projections on the development of pension distributions;

- value of accrued pension rights and an equilibrium calculation of the earnings-related pension scheme; and

- an internal return calculation, which shows how much different age cohorts and generations get in return for their pension contributions.