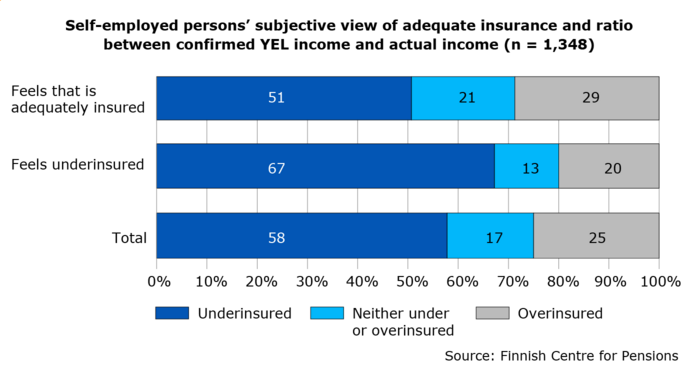

More than half of the self-employed feel that they have insured themselves adequately

Of the self-employed, 57 per cent feel that they pay adequate pension contributions, while 43 per cent feel they have underinsured themselves. A recent study by the Finnish Centre for Pensions shows that the majority of the self-employed pay low contributions in relation to their income.

Of the self-employed, 57 per cent feel that they pay adequate pension contributions, while 43 per cent feel they have underinsured themselves. A recent study by the Finnish Centre for Pensions shows that the majority of the self-employed pay low contributions in relation to their income.

The confirmed income under the Self-employed Persons’ Pensions Act (YEL income) that forms the basis of pension insurance for the self-employed, is usually underdimensioned when compared to the actual income of the self-employed. For approximately every second self-employed person who took part in the study, the confirmed YEL income was only 80 per cent of their actual income.

In this study, a self-employed person was considered underinsured if their YEL income was at least 10 per cent (or €2,400) below their actual annual income. Based on this indicator, more than three out of five underinsured themselves, economist Satu Nivalainen explains.

The opposite, in which the YEL income exceeded the actual income by at least 10 per cent (or 2,400 euros), was the case for every fourth self-employed person in 2017.

In addition to the future pension, the confirmed YEL income forms the basis for other earnings-related social security, such as the sickness and unemployment allowances, of the self-employed.

”In light of the study results, the YEL income of one quarter of the self-employed was so low that they run the risk of not having the right to earnings-related social benefits,” Nivalainen explains.

Self-employed aware of underinsuring themselves

According to the study, the problems with underinsurance concern a few groups of self-employed persons. Self-employed without employees and self-employed persons without copartners both feel that they pay too little in pension contributions and actually underinsure themselves. The same applies to self-employed persons who have too much work and a meagre income.

Self-employed with employees and self-employed persons with copartners, on the other hand, often feel that they have insured themselves adequately. Compared to their actual income, they pay adequate pension contributions. Typically, they work for less than 50 hours a week, do not have too much work and have accrued pension also from a career as wage earners.

“Underinsurance based on actual income is more common among the young self-employed and those with a basic education. Correspondingly, older and highly-educated self-employed persons overinsure more often than others,” economist Sanna Tenhunen states.

Cannot afford to pay higher pension contributions

The study also reviewed the reasons for underinsurance among the self-employed.

The most common reason is that the self-employed cannot afford to pay higher insurance contributions. Two out of three self-employed were of this opinion.

The following most common causes were lack of trust in the pension system and work intentions. About half of the self-employed reported that they underinsured themselves because they suspect that they will not get an adequate pension regardless. Equally many stated that they plan to work alongside drawing a pension.

Research data of more than 1,000 self-employed persons

The study focused primarily on full-time, active self-employed persons. The study comprised the data of 1,348 self-employed persons. The income from self-employment included both the wage income paid by the self-employed to themselves and their taxable earnings from self-employment. To even out annual fluctuation, we used the average income over a period of three years.

The data is based on the Ad hoc module of self-employment compiled in connection with Statistics Finland’s 2017 Labour Force Survey (LFS). We have combined this data with income data from Statistics Finland and pension accrual data from the registers of the Finnish Centre for Pensions.

Three facts about the YEL income

- The YEL income is confirmed by the earnings-related pension provider when the self-employed person takes out statutory pension insurance.

- In addition to the pension amount, the self-employed person’s daily allowance under health insurance and the compensation under voluntary worker’s occupational insurance are determined based on the confirmed income. The confirmed income also affects the unemployment allowance and income during maternity, paternity and parental leaves.

- Rule of thumb: the confirmed income should correspond to the wage that a self-employed person would pay to a worker hired to do the same work.