Size or content of the pie – amount and source of income is related to income perceptions

European pensioners get the main part of their income from pensions, but also from work, capital, and other social benefits than pensions. Our recent study shows that the perceived income adequacy depends not only on the amount but also on the source of income.

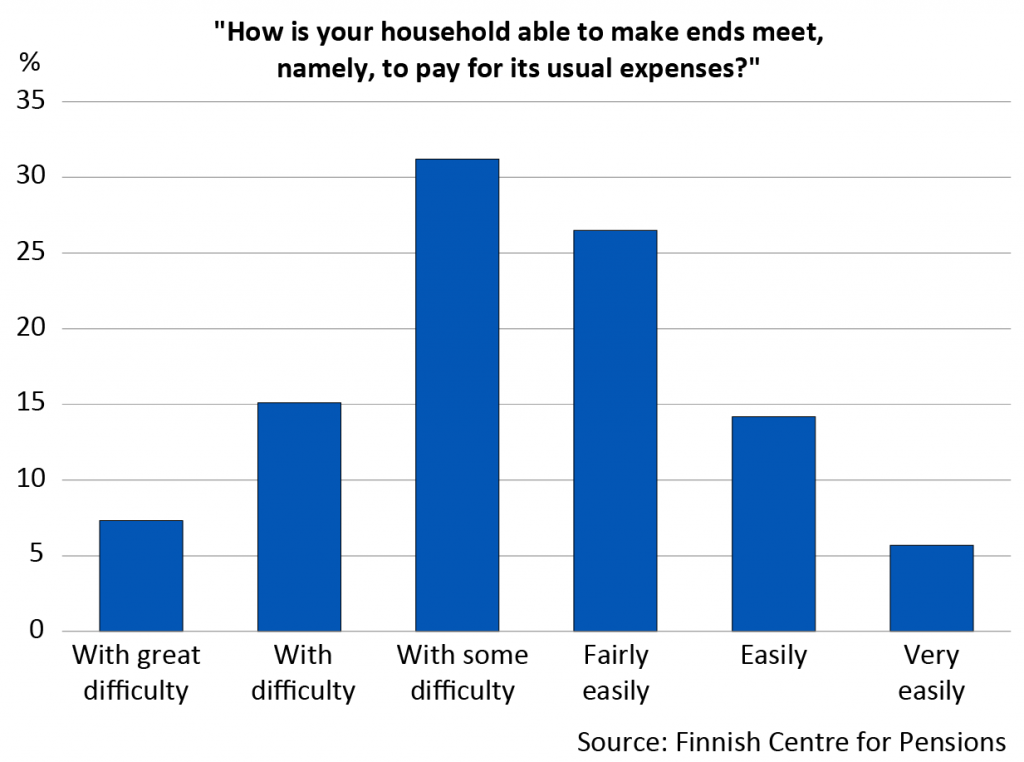

Pensioners’ perceived financial situation is important since income alone does not indicate whether they feel they can make ends meet. European pensioners said that they can cover everyday expenses reasonably well for the most part. Slightly less than one third of pensioners experienced some problems with covering their expenses while an ample one fourth found it fairly easy to make ends meet.

Nearly one in ten Finns experienced some difficulties and one in three found it fairly easy to cover everyday expenses. In our research article published in the Journal of Aging & Social Policy, we examined the importance of income sources for perceived income adequacy in retirement based on the EU-SILC (European Union Statistics on Income and Living Conditions) survey conducted in 29 countries.

Pensions contribute to experience of income adequacy; earnings from work weaken the experience

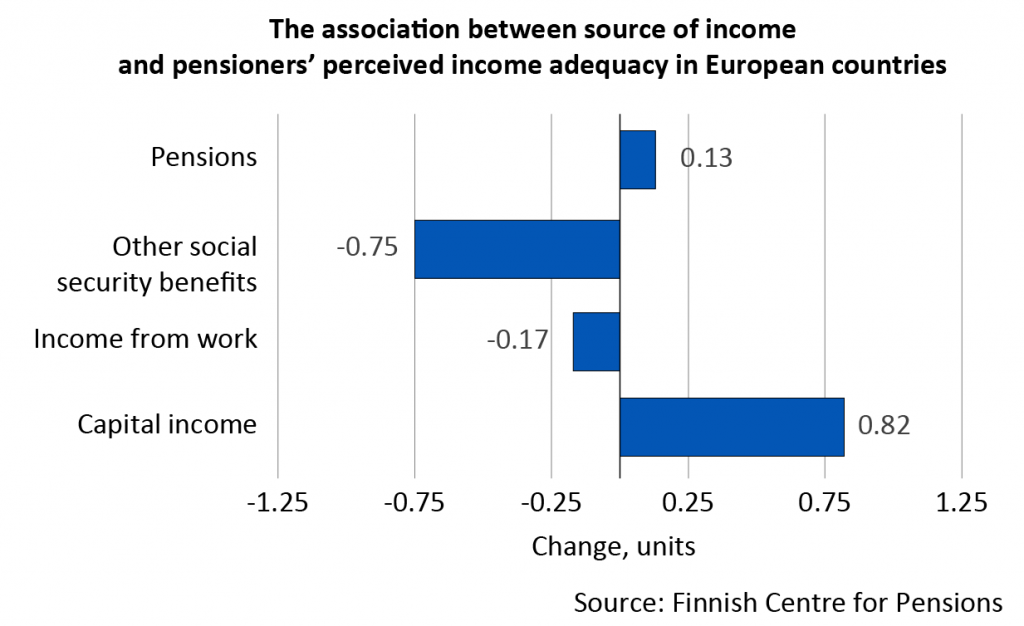

The results of our study on the association between income sources and pensioners’ subjective economic well-being are interesting because this research question has not been posed before. When there are no differences in the other household characteristics (for example, in income level), the income is perceived to cover expenses better, the bigger its share that stems from pensions.

Capital income is associated with higher perceived income adequacy in the same way as pensions – the larger the share of capital income, the better the income is perceived to cover expenses. Social security benefits other than pensions, on the other hand, are associated with the income experience negatively. The same applies to income from work, although to a lesser degree.

What do the results tell us?

The results make us reflect on their underlying causes. Pensions are a regular source of income and do not have to be repeatedly claimed. This provides income security and makes it easier for pensioners to plan their spending. The assessment may also reflect that people perceive pensions as income they deserve after working life.

Capital income plays a significant role for those lower income groups who receive it. Capital can generate extra income and offer security particularly for those in a weaker financial situation.

If work is compulsory for financial reasons, that is, not done by choice or part-time as for pensioners in general, the income from work may be perceived less adequate. The perception may also be about consumption preferences.

Applying for other social security benefits than pensions, on the other hand, may involve uncertainty, bureaucracy and stigma. This, in turn, may weaken the income adequacy perception of social security benefits compared to income from other sources.

Less than one fifth of pensioners’ income comes from sources other than pensions

- On average, European pensioner households get 82 per cent of their income from pensions.

- The share of income from work is nine per cent.

- The share of capital income (for example, rental income) is five per cent.

- The share of income from benefits other than pensions (for example, housing allowance) is four per cent.

- The share of income that stems from work and capital is clearly larger for higher income groups while lower income groups receive more income from social security benefits other than pensions.

Our study covers 29 countries and is based on data from the EU-SILC (2018) survey.

Read the research article:

Size or Content of the Pie? Source of Income and Perceived Income Adequacy of Older Europeans. Journal of Aging & Social Policy 2022

How much pension do they get on average? Do retirees in Europe feel satisfied with the results of their retirement?

Tel-U