International pension comparison: Finnish pension system ranks eighth – tops the integrity sub-index

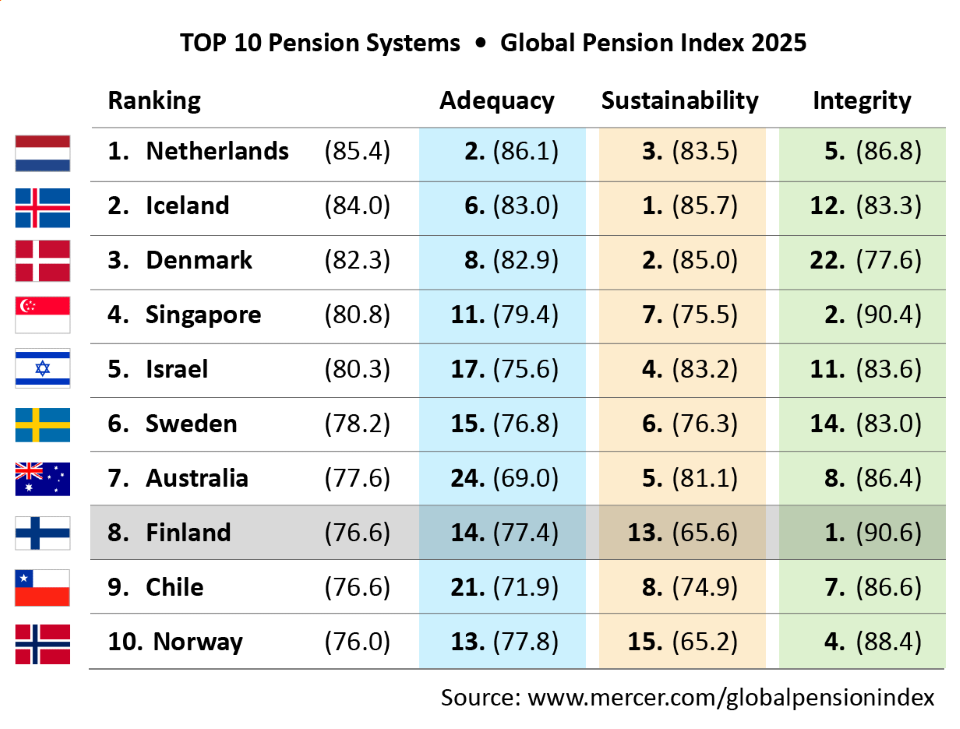

This year, Finland ranked eighth in the international Mercer CFA Institute Global Pension Index comparison. Finland dropped one notch compared to 2024. Finland continues to be rated as having the most reliable pension system governance in the world.

The Finnish pension system is regarded internationally as reliable and stable, and for a long time, it has received high marks in the world’s most comprehensive pension system comparison.

Finland’s total score in the Mercer comparison improved slightly this year. Yet the rise was not enough.

“This time, almost all countries saw an increase in their scores, some quite significantly. This is due not only to pension reforms implemented in various countries, but also to adjustments in the indicators used. Despite its strong performance, Finland dropped one notch”, says Liaison Manager Mika Vidlund (Finnish Centre for Pensions).

Mercer benchmarks the retirement income systems of various countries using adequacy, sustainability and integrity as sub-indices. Director Allan Paldanius (Finnish Centre for Pensions) considers Finland’s overall score to be quite strong.

“Compared to the other countries in the top ten, Finland faces more challenges in terms of financial sustainability and the adequacy of pension provision, though the differences between countries are not significant. In contrast, Finland excels, even serves as a model, when it comes to the integrity sub-index.”

According to Mercer, the most financially sustainable pension systems are found in Iceland, Denmark, and the Netherlands. What these countries have in common are fully funded, defined contribution pension schemes that cover most of the working-age population.

Exceptionally efficient administration in Finland – pensions accessed through a single point of contact

Mercer’s assessment of the administration of Finland’s pension system remains unchanged: once again, Finland receives the highest marks in the world.

For citizens, this is evident in how easy it is to claim a pension. Here, the old-age pension can be accessed quickly and simply through a single point of contact. In many other countries, pensions are fragmented across different institutions, requiring individuals to claim each component separately,” explains Paldanius.

When evaluating the integrity of a pension system, Mercer considers factors such as its operational effectiveness, transparency and regulation, and the reasonableness of its administrative costs.

Sweden overtook Finland

From a Nordic perspective, Mercer’s annual comparison brings a major surprise. Until now, Finland’s pension system has consistently scored better than Sweden’s. However, Sweden has now overtaken Finland.

Vidlund identifies several reasons for Sweden’s rise.

“In terms of sustainability, Sweden has always been among the top countries in the comparison, but overall, it has still been the weakest among the Nordic nations. This has not gone unnoticed in the Swedish media either, and there has been pressure for reforms for quite some time.”

This year, Sweden has caught up in both the adequacy of pension provision and the financial sustainability of the system, but its position has particularly strengthened with regard to the reliability of administration.

“Recently, Sweden has implemented several significant reforms. The governance and investment rules for the AP buffer funds have been updated, risk management in occupational pension companies has been reinforced, and responsibilities within governance have also been clarified.”

What is Mercer?

The Mercer CFA Institute Global Pension Index comparison is compiled by Mercer, an international consultancy firm, that benchmarks the retirement income system’s of different countries with the help of more than 50 indicators.

The countries’ total scores are calculated using a weighted average. The weightings used are 40 per cent for the adequacy sub-index, 35 per cent for the sustainability sub-index and 25 per cent for the integrity sub-index.

This year, 52 countries took part in the comparison, representing two-thirds of the world’s population. Kuwait, Namibia, Oman, and Panama participated for the first time.

The Global Pension Index report has been published since 2009.

Mercer’s recommendations for pension investors and governments

Pension fund investments require balancing between the pension fund participants’ best interest and the national interest, explains the international consultancy firm Mercer in its recent annual report.

Governments around the world influence, and in many instances, restrict pension funds’ investments. Increased global uncertainty and the increasing size of pension fund assets are now leading some governments to consider encouraging more domestic investment by pension funds in areas of national priority for the longer-term benefit of society.

Mercer recommends eight principles for governments to intergrate different interests.

- Retirement first. The primary purpose of a pension fund is to provide retirement income to the fund’s participants and their dependants.

- Fiduciary integrity. Fiduciaries must act in the best interests of the pension fund’s beneficiaries.

- Robust governance. Pension legislation should require all pension funds to develop a comprehensive investment policy and follow sound investment governance practices.

- Full market access. Pension funds must consider the full range of available investment opportunities appropriate for their size and complexity, recognizing that available opportunities are impacted by a country’s economic development.

- Policy incentives, not mandates. Governments can make particular investments attractive to pension funds without the use of compulsion. The actual investment decision should be left to the pension fund.

- Collaborative scale. Pension funds should collaborate with each other and with the government to increase investment opportunities, for example, infrastructure projects.

- Transparency, not constraints. There should be transparent public disclosure relating to the actual investments held and their returns and risks, but no performance tests or fee caps should be applied to pension fund investments.

- Macro awareness. When private pension fund assets are a significant percentage of GDP, governments must recognize the impact and interactions between their fiscal and social policies and the implications for present and future retirees.

Read more: