Financial statement and cost of division figures

The year 2024 return on investments on the private sector yielded 9.1 per cent and pension assets increased by 12.2 billion euros. Public sector investments yielded 9.6 per cent and pension assets increased by 7.3 billion euros. All investments yielded 9.3 per cent.

A certain obligation to transfer into funds has also been determined for pension providers with TyEL and MEL activities. In 2024 fund transfer obligation was 6.8 per cent. On the grounds of that pension providers must level their own technical provision. The higher the solvency levels are, the higher the fund transfer obligation is and vice versa.

(Updated on 3 June 2025)

Statistical tables:

- Financial statement figures in Statistical database of the Finnish Centre for Pensions

- Cost of division figures in Statistical database of the Finnish Centre for Pension

Financial statement and cost of division figures

Producer: Finnish Centre for Pensions

Website: Financial statement and cost of division figures

Subject area: Financing and Insurance

Part of the Official Statistics of Finland (OSF): No

Description

The statistic offers a general overview how pension providers operate. With the help of the statistic it is easy to compare pension providers financial statement and cost of the division figures from different years.

Data content

The table presents figures from the financial statements of private and public-sector pension providers of the earnings-related pension scheme. The figures concern earnings-related pension insurance, investment operations, claims paid, administrative expenses, technical provisions and solvency.

Categorizations

Pension scheme TyEL, MEL, YEL, MYEL, municipals, state, church, others (include Kela and Bank of Finland).

Methods of data collection and source

The data has been compiled partly electronically from the the pension providers’ financial statements and cost of division figures.

Update frequency

Twice a year.

Time of completion or release

Financial statements figures in June following the statistical year. Cost of division figures in October following the statistical year.

Time series

The statistical data is available from 2007 onwards.

Key words

Pension assets, insurance contributions, investment profits, claims paid, total operating expenses, solvency, techincal provision.

Financial statement figures

Numbers

The table presents general information on the number of pension providers within the private- and public-sector earnings-related pension scheme and the pension provision they manage in the form of numbers of insurance policies, insured, pension recipients and rehabilitees.

Pension providers is the number of pension providers at year-end of the statistical year.

Number of insurance policies is the number of insurance contract policies. The number is a pension providers estimation at year-end.

Number of insured is at year-end number of insured. A person can have at the same time several employments.

Pension recipients is at year-end number of pension recipients. A person can receive pension from several pension provider. The number is a pension providers estimation at year-end.

Rehabilitees is the number pension providers have informed to Finnish Center for Pensions for statistical use. The number of rehabilitees includes rehabilitees who have received income compensation.

Premium income

The table presents the premium income, of private- and public-sector pension providers within the earnings-related pension scheme, divided into employer and employee contributions, contributions paid by the self-employed and the State’s component. In addition, the contribution from the Employment Fund, transition contribution income and the wage sum are presented.

Employers’ contribution is the employers’ share of the premium written on the financial year. Employers report the earnings of their employees to the pension providers. The employer withholds the wage earner’s share of the contribution straight from their wages and pays the entire insurance contribution to the pension provider. The contribution rates are prepared and confirmed according to praxis set out in each separate pension act. The exact amount of the collected pension contributions for each year is known only later, once the employers report their realised contribution and wage sums.

Employees’ contribution is the employees’ share of the premium written on the financial year. An employee’s contribution depends on age. Employees’ under 53 and above 63 pay lower contribution.

Entire wage earners’ contribution contains both employers’ and employees’ contributions.

Self-employed persons premium

The earnings-related pension contribution for self-employed person is calculated as a per cent of their insured confirmed income. The farmers insurance contribution is calculated based on the personal MYEL income of the insured. The contribution rate depends on the insured’s age and amount of income.

State’s component

The state covers the share of pensions paid under the pension acts for the Self-employed (YEL and MYEL) that the collected insurance contributions do not cover.

Slightly less than one third of the MEL pension expenditure is financed from the state budget.

The State pensions are paid from reserved funds in the state budget. Assets collected through pension contributions are transferred annually from the State Pension Fund to the budget to an amount corresponding to approximately 40 per cent of the actual pension expenditure. The additional 60 per cent is paid straight from the state budget for the year in question.

Contribution from TR

The advance contributions and previous year’s adjustment contributions have been taken into account in the contribution from the Employment Fund.

The contribution of the Employment Fund is used to pay for costs incurred from the pension accrued from periods of unemployment and education, as well as based on benefits received during periods of job alternation leave. The Employment Fund pays the Finnish Centre for Pensions a contribution that the Finnish Centre for Pensions reimburses to the TyEL pension providers, the Seafarers’ Pension Fund, municipals, church, Kela and the Bank of Finland.

The Employment Fund also pays a separate contribution to the State Pension Fund.

Transition contribution income

Transition contribution income is paid by pension providers in the private sector to the state. Transition contribution is determined when state agencies, institutions or public utilities become shareholding companies or if their operations are transferred to existing shareholding companies.

Total premium income contains entire wage earners’ contribution, contribution from TR and transition contribution income.

YEL, MEL, MYEL and state contain also the State’s component.

The Wage sum/Earned income are a pension providers estimation at year-end. The exact amount of the collected pension contributions for each year is known only later, once the employers report their realised contribution and wage sums.

Return on investments

The table presents the return on investments of private- and public-sector pension providers within the earnings-related pension scheme at book value and fair value, the pension providers’ capital employed and the rate of return on the capital employed.

The return on investments at fair value is calculated by adding the adjustment in the difference between fair value and book value that year. When the resulting figure is deducted by the investment charges at book value, we get the net investment income at fair value.

Capital employed is a market-valued investment. The capital employed is calculated by adding to the market value at the beginning of the financial year the cash flows of the financial year weighted with the relative share of the length of the total financial year left from the transaction date to the end of the financial year.

By dividing the net investment income with the capital employed, we get the rate of return for the capital employed.

Claims paid

The table presents pensions and compensation for division of costs paid by the private- and public-sector pension providers within the earnings-related pension scheme. The data is divided based on the paying pension provider.

Administrative costs

The table presents total operating expenses of private- and public-sector earnings-related pension providers within the earnings-related pension scheme.

The statutory payments of the total operating expenses have also been specified in the table.

The advance premiums of the statistical year and the adjustment contribution of the previous year have been taken into account in the costs of the Finnish Centre for Pensions.

The administrative expenses of investments are not included in the figures. They are included in the investment income and investment charges when calculating the investment income at book value.

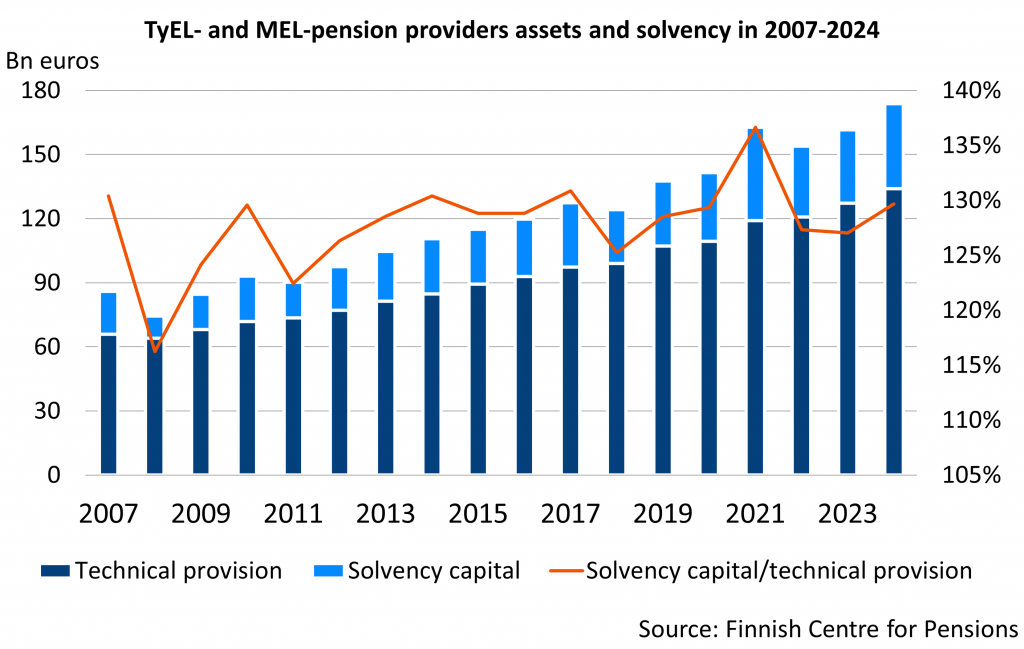

Pension assets

The table presents the pension assets, the investments and the investment allocation of private- and public-sector pension providers within the earnings-related pension scheme.

As of the beginning of 2013 private-sector pension assets include the technical provisions added to the solvency capital. Private-sector pension assets 2007-2012 include the technical provisions added to the solvency margin.

The investment assets are presented as pension asset for the public-sector. As the public-sector lacks technical provisions.

Investments are presented at fair value. The investment assets are allocated (%) into interest, equity and real estate and other investments.

Solvency

The table presents the solvency margin, solvency ratio, solvency limit and solvency position of private-sector pension insurance companies, industry-wide pension funds and company pension funds within the earnings-related pension scheme.

The solvency margin is a solvency key figure until 31.12.2012. The solvency margin consists of the company’s capital and reserves, the difference between the fair value and book value of assets, the provision for future bonuses and the depreciation difference, reduced by intangible assets. The solvency margin is used to balance the investment risks.

Equalisation provision is part of the solvency capital as of the beginning of 2013. Equalisation provision is a buffer fund for the insurance business that is used to provide for losses incurred in the insurance business. At the beginning of 2017, the equalisation provision, was incorporated in the provision for future bonuses.

Due to the crisis on the international financial markets, the regulations concerning the investment operations and solvency of pension providers were amended for a fixed-term period from 2008 to 2012. In order to strengthen the solvency of pension providers, the provision for pooled claims included in the technical provisions was temporarily made comparable with the solvency margin.

The solvency capital, as of the beginning of 2013. Pension insurance companies and industry-wide pension funds have merged the buffer for investment risks, i.e. the solvency margin, and the buffer for the insurance business, i.e. the equalisation provision, to create one common buffer, the solvency capital. At the beginning of 2017, the equalisation provision, was incorporated in the provision for future bonuses.

Technical provisions used for calculating solvency is until 31.12.2012 technical provisions minus the provision for pooled claims comparable with the solvency margin and the provision for future bonuses. As of the beginning of 2013, the provision for future bonuses and the equalisation provision are deducted from the technical provisions when solvency is calculated.

The solvency ratio until 31.12.2012 is calculated by dividing the solvency margin with the technical provisions used in calculating the solvency. As of the beginning of 2013, the solvency ratio is calculated by dividing the solvency capital by the technical provisions used for calculating solvency.

The solvency limit is a variable calculated on the basis of the investment portfolio structure and the amount of the technical provisions. The solvency limit has been dimensioned so that there is a high probability that some of the solvency margin will still exist a year later, taking into account the distribution of investments into different asset categories. The minimum solvency capital is one thirds of the solvency limit, while the maximum solvency capital is four times the solvency limit. In 2008-2012, the minimum solvency margin for earnings-related pension 1 per cent insurance companies was 2 per cent and for industry-wide pension funds and company pension funds of the technical provisions.

The solvency position (the z figure) until 31.12.2012 is calculated by dividing the solvency margin with the solvency limit. As of the beginning of 2013, the solvency position is the solvency capital in relation to the solvency limit.

Technical provisions

The table presents the technical provisions of private-sector earnings-related pension insurance companies.

The technical provision is the insurance company’s estimated future pension expenditure insofar as it has been funded, reported in the financial statements.

The technical provisions is divided to provision for unearned premiums and provision for claims outstanding.

The provision for unearned premiums applies to all liabilities arising for providers from future pension contingencies to the degree that pension has accrued by the end of the financial period.

By provision for claims outstanding is meant the capital value of funded shares of old-age, disability and unemployment pensions that will be paid in the future from pension contingencies that have already occurred.

Cost of division figures

Claims paid

The table presents pensions and compensation for division of costs paid by the private- and public-sector pension providers within the earnings-related pension scheme. The data is divided based on the paying pension provider.

The advance premiums of the statistical year and the adjustment contributions of the previous years have been taken into consideration in the compensation for division of costs.

TEL-L supplementary pensions are included in the compensations of TyEL’s division of costs.

The minus sign in compensations means the pension provider’s receivables from the Finnish Centre for Pensions, while the plus sign means the payments due to the Finnish Centre for Pensions in the division of costs.

Technical provisions

The table presents the technical provisions of private-sector earnings-related pension insurance companies.

The technical provision is the insurance company’s estimated future pension expenditure insofar as it has been funded, reported in the financial statements.

The technical provisions is divided to provision for unearned premiums and provision for claims outstanding.

The provision for unearned premiums applies to all liabilities arising for providers from future pension contingencies to the degree that pension has accrued by the end of the financial period.

Provision for current bonuses is part of the provision for unearned premiums. Certain portions of the investment surplus and loading profit have been transferred to the provision for current bonuses on the basis of the company’s solvency status. Reserved for the payment of client bonuses the following year.

Provision for future bonuses is part of the provision for unearned premiums. It is used as a measure to prepare for investment value fluctuations. It is included in the company’s solvency capital.

Equity-linked provision for current and future bonuses is part of the provision for unearned premiums. A buffer jointly maintained by earnings-related pension companies bearing some of risks resulting from fluctuations in equity income.

By provision for claims outstanding is meant the capital value of funded shares of old-age, disability and unemployment pensions that will be paid in the future from pension contingencies that have already occurred.

Current disability- and unemployment pensions are divided to known and unknown pensions.

Provision for pooled claims is a common buffer for earnings-related pension companies.The buffer ensures the adequacy of financing for jointly covered pension components even in poorer economic circumstances.

Equalisation provision is part of the provision for claims outstanding. It is accumulated amount from the risk business result used to equalise any fluctuations in the technical underwriting result or for years when number of new pensions granted is higher than estimated at the time of when contributions were determined. The equalisation provision is divided into sub-sections old-age pension movement, disability pension movement and contribution loss movement.

At the beginning of 2017, the equalisation provision, was incorporated in the provision for future bonuses.