System Description

Pension insurance provides a secure income against various long-term risks. The national pension covers all people residing in Finland if they meet the minimum requirements relating to time of residence. Earnings-related pensions cover people with earned income.

In Finland, earnings-related pensions accrue for nearly all gainful employment. There are several earnings-related pension acts. Wage earners get earnings-related pensions mainly under the Employees Pensions Act (TyEL), the Seafarer’s Pensions Act (MEL) and the Public Sector Pensions Act (JuEL). The Public Sector Pension Act (JuEL) was created in 2017 when the Local Government Pensions Act, the State Employees’ Pensions Act, the Evangelical-Lutheran Church Pensions Act, Bank of Finland and the regulations concerning the earnings-related pensions of the employees of Kela merged.

The earnings-related pension scheme covers all employees, self-employed persons and farmers whose employment exceeds the minimum requirements laid down by law. Self-employment is insured either under the Self-employed Persons’ Pensions Act (YEL) or the Farmers’ Pensions Act (MYEL).

In the private sector, pensions are arranged mainly through insurance policies. In the public sector, wage earners are automatically covered via their employer under public sector pension acts.

In addition to these, pensions are paid based on the Motor Liability Insurance Act, the Workers’ Compensation Act, the Act on Compensation for Military Accidents and Service-Related Illnesses and the Act on Compensation for Accidents and Service-Related Illnesses in Crisis Management Duties.

The national pension and the guarantee pension secure a basic livelihood if the retiree has accrued no or only a small earnings-related pension.

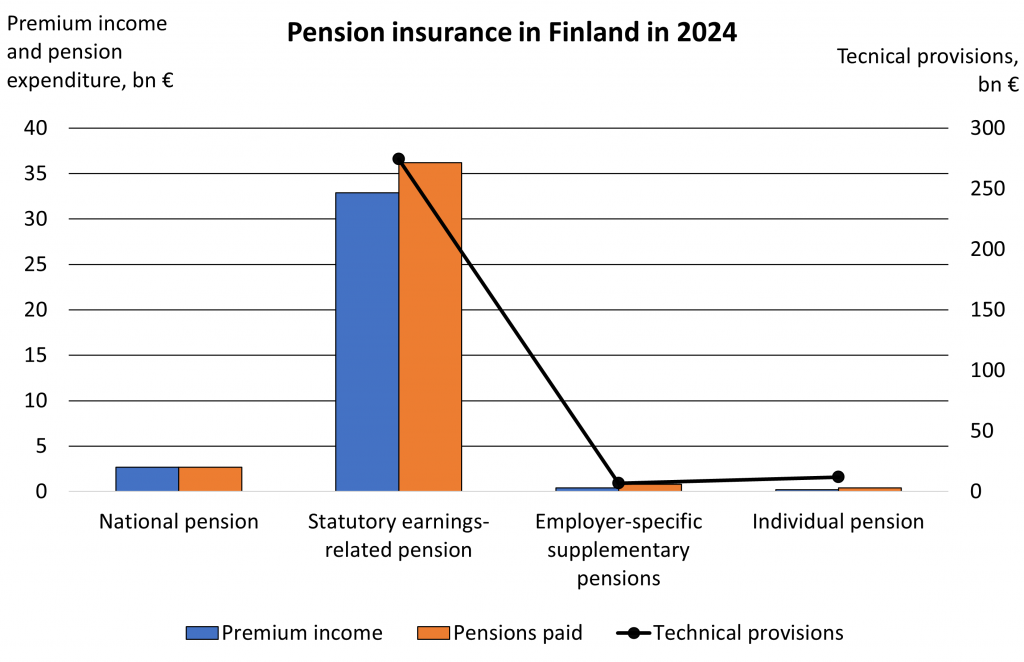

Compared to many other European countries, employer-specific or voluntary pensions or pensions based on labour market agreements are rare in Finland. This is because, among other things, there is no pension ceiling or upper limit to the amount of earnings that the pension is based on in the statutory pension system.

Administration

The administration of the earnings-related pension scheme is decentralised. In the private sector, earnings-related pensions are handled by earnings-related pension insurance companies, industry-wide pension funds, company pension funds, farmers’ and seafarer’s special pension insurers. They are all coordinated by the Finnish Centre for Pensions and supervised by the Ministry of Social Affairs and Health and the Finnish Financial Supervisory Authority. Public sector pensions are managed mainly by one pension provider (Keva). Earnings-related pension providers grant an pay out pension and offer guidance for the insured. Employers and the self-employed pay their pension contributions to the pension providers.

Kela manages the national pension system. In addition to national pensions, Kela handles other social benefits, as well. National pensions are financed with state funds.

Earnings-related pensions are part of statutory social security and financed with pension contributions based on earnings from work or self-employment. Constitutional protection of property applies to earned pension rights. The integrity of the accrued earnings-related pension is ensured by collecting all employment and self-employment data into the registers of the Finnish Centre for Pensions and the pension providers. The pension providers are jointly liable for meeting the pension promises. In the Finnish earnings-related pension system, the right to a pension remains even when the employer changes.

Earnings-related pension scheme

Pension accrues for work carried out from the age of 17 until the age of 68, 69 or 70 depending on the birth year of the person. For the self-employed, pension benefits accrue as of age 18. The pension is calculated based on the person’s earnings for each year and an age-specific accrual rate. Pension also accrues based on certain unsalaried periods, such as periods of unemployment or study. Benefits paid out in connection with pensions also accrue for studies that leads to a degree.

The earnings-related pension index is used to revalue the euro amounts of pensions in payment at the beginning of January each year. The wage coefficient has been used as of 2005 to calculate pensions and to revalue earnings from work, self-employed persons’ confirmed income and the limit amounts laid down in the acts on the earnings-related pension.

Changes in life expectancy will affect starting pensions through the life expectancy coefficient. The purpose of the coefficient is to control the growth of pension expenditure as people live longer and to encourage people to continue working.

As life expectancy rises, the life expectancy coefficient reduces the monthly pension. It does not reduce the total pension amount paid throughout the time of old-age pension if the pension recipient lives to the age of the expected life expectancy.

The national pension scheme

The national pension and the guarantee pension secure a basic livelihood if the retiree has accrued no or only a small earnings-related pension. Kela pays out the national and the guarantee pensions.

In 2026, the full amount of the monthly national pension for a single person is 787.07 euros and for a married or cohabiting person 702.69 euros.

National pensions include old-age, disability, surviving spouse’s and orphans’ pensions, in addition to rehabilitation benefits.

The national and earnings-related pensions are integrated into a total pension. Every euro of earnings-related pension reduces the national pension by 50 cents until, at a certain level of the earnings-related pension, no national pension is granted.

Guarantee pension

The guarantee pension improves the income of those with the lowest income. If the national and earnings-related pension of the pension recipient is below the pension income limit defined by law, the difference is supplemented with the guarantee pension. In 2026, the pension income limit of the guarantee pension is 990.90 euros per month.

Other pension income reduces the guarantee pension in full (100%). Pension income reduces the guarantee pension more than the national pension. All pensions, including survivors’ and farm closure pensions, paid in Finland and from abroad affect the amount of the guarantee pension.

Pension financing

In Finland, statutory earnings-related pensions are financed mainly through the pay-as-you-go (PAYG) system, that is, the earnings-related pension contributions paid in the year in question. Part of the pensions are financed under the partial funding principle by using both earnings-related pension contributions and previously accumulated funds.

Contributions under TyEL and MEL are paid jointly by the employer and the employee. Part of the TyEL and MEL contributions are funded into funds governed by the earnings-related pension providers. Contributions under YEL and MYEL are paid in their entirety by the self-employed. The State participates in the financing of MEL pensions with just under one third of the pension expenditure and of the pensions of the self-employed to the extent that the insurance contributions are not sufficient to cover the pension expenditure.

The contributions paid by the self-employed are not funded. Public sector earnings-related pensions are financed under the PAYG principle, with the support of buffer funds.

Kela pensions are financed by the State.

Earnings-related pension benefits

Within the earnings-related pension scheme, it is possible to retire on an old-age pension flexibly between the cohort-specific retirement age and the age at which the insurance obligation ends. Following the pension reform in 2017, the retirement age rises gradually from 63 to 65 years with 3 months per age group. After that the retirement age will be linked to life expectancy.

The first age group whose retirement age rose were those born in 1955. For those born in 1965 or later, the old-age retirement age will be linked to the rising life expectancy. For those born in 1957 or earlier, the insurance obligation ends at age 68; for those born between 1958 and 1961, it is 69 years; for those born in 1962 or later, it is 70 years.

In the public sector of the earnings-related pension scheme, it is possible for the so-called ‘old workers’ to retire according to earlier agreement at an individual or occupational retirement age. Under MELA, it is possible to retire at an earned retirement age.

From the beginning of 2017, it has been possible to retire on an earnings-related partial old-age pension. This pension is available to persons born in 1949 or later who have reached the qualifying age for the benefit, determined based on year of birth. Eligible persons may not receive any other pension in their own right at the start of the partial old-age pension. The amount of partial old-age pension is 25 or 50 per cent (based on the individual’s own choice) of the earnings-related pension accrued at the time of retirement. An early retirement reduction is made to the pension if it is taken out before the retirement age of the age group concerned. There are no rules regarding employment; partial old-age pension recipients may continue to work if they want to.

In the national pension scheme, the age limit for the old-age pension is 65 years for those born in 1962 or earlier. After that the retirement age is the same as in the earnings-related pension scheme. Persons born before 1962 can take out their national old-age pension early: persons born before 1958 at the age of 63 years persons born between 1958 and 1961, it is 64 years. Early retirement reduces the pension permanently.

Retirement on old-age pension can also be deferred. The earnings-related old-age pension is increased if taken out late, after reaching the retirement age. Under the national pension scheme, the age threshold for the increase is 65 years for now.

A disability pension can be granted to a person who suffers from a disease that reduces the person’s work ability. Besides health, the person’s possibilities of earning a living (by such available work which the person can reasonably be expected to manage when taking into account their education and training, age, previous activities, living conditions and other comparable factors) are considered. In the public sector it suffices that, due to an illness, a handicap or an injury, the person has become incapable of doing their own job. When assessing whether a 60-year-old person with a long work history is entitled to a disability pension, the occupational nature of the work inability is emphasized especially.

An earnings-related pension provider can grant a disability pension to a person who has turned 17 years and who has not reached the age group’s retirement age. The disability pension is converted into an old-age pension when the pension recipient reaches their retirement age.

In the national pension scheme, the disability pension may be granted to persons aged 18–64 years.

In the earnings-related pension scheme, it is further required that the work inability can be estimated to last for at least one year. In the national pension scheme, the pension is not awarded to persons under the age of 20 until their possibilities of rehabilitation have been investigated. A permanently blind person or a person unable to move is always considered disabled in the national pension scheme.

The disability pension may be awarded either until further notice or as a fixed-term cash rehabilitation benefit. The cash rehabilitation benefit is granted if it can be expected that the person’s ability to work can be restored at least in part through treatment or rehabilitation. The granting of a cash rehabilitation benefit always requires a treatment or rehabilitation plan.

The earnings-related disability pension may be awarded as a full pension or a partial pension. A person is granted a full disability pension if their ability to work is considered to have been reduced by at least 3/5 and a partial disability pension if their ability to work is considered to have been reduced by 2/5 – 3/5. The partial disability pension is half of the full disability pension. A disability pension paid under the national pension scheme is not granted as a partial pension.

In the earnings-related pension scheme, the disability pension can also be granted as a years-of-service pension if the pension applicant has done work that requires great mental or physical effort for at least 38 years. In addition, the applicant’s ability to work must be reduced, but less so than for the actual disability pension. The first years-of-service pensions were paid out in 2018.

The survivors’ pension may be paid to the children, the surviving spouse or a former spouse of the deceased insured person.

Children are entitled to the orphan’s pension if they are under the age of 20 at the time of the death of the insured parent. In the national pension scheme, children aged 18–20 are also entitled to an orphan’s pension if they are full-time students or participate in vocational training (student’s pension).

Children entitled to the orphan’s pension are the biological or adopted children of the deceased person, of the surviving spouse, and of the partner in a registered partnership.

A married surviving spouse is entitled to the surviving spouse’s pension if:

- the surviving spouse has, or has had, a child (biological or adopted) together with the deceased and the spouses married before the deceased reached the age of 65; or

- the spouses married before the deceased reached the age of 65 and the surviving spouse reached the age of 50, the marriage had continued for at least five years, the surviving spouse has reached the age of 50 at the time of the spouse’s death, or the surviving spouse has been long-term disabled.

A common-law surviving spouse is entitled to a surviving spouse’s pension if all the following criteria are met:

- The deceased spouse died in 2022 or later.

- The surviving common-law spouse has a dependant child under the age of 18 together with the deceased spouse.

- The common-law spouses lived in the same household for at least five years before the other spouse died.

- The common-law spouses moved into a shared household before the deceased spouse turned 65.

- Neither common-law spouse was married to another person.

Within the earnings-related pension system, the survivor’s pension can also be granted to a former spouse of the deceased person or to the party of a dissolved registered partnership if the deceased was liable to pay alimony to the spouse or partner at the time of death.

A surviving spouse who was married to the deceased person receives the surviving spouse’s pension for the rest of their life if the surviving spouse was born before 1975 or if the spouse passed away before 1 January 2022. A surviving spouse born in 1975 or later will be paid the surviving spouse’s pension for 10 years or until the youngest of the children receiving an orphan’s pension turns 18.

A common-law surviving spouse will be paid the survivor’s pension until the youngest of the shared children turns 18. If the surviving spouse remarries before reaching the age of 50, the surviving spouse’s pension ends.

If a surviving spouse under 50 years of age remarries, the surviving spouse’s pension is terminated.

Earnings-related pension acts

Private sector

TyEL Employees Pensions Act

MEL Seafarer’s Pensions Act

YEL Self-Employed Persons’ Pensions Act

MYEL Farmers’ Pensions Act

Public sector

JuEL Public Sector Pensions Act

OrtKL Orthodox Church Act

Pension regulation for the regional government of Åland

National pension acts

KEL National Pension Act

REL Front-Veterans’ Pensions Act

URL Act on Front-Veterans’ Supplement Payable Abroad

Pension part of social security

The aim of the Finnish social security system is to ensure basic security for everyone in all situations in life. Social security can be divided into social insurance and social and health services.

There is both statutory social insurance and supplementary allowances. Social insurance refers to statutory measures taken to secure the livelihood of an individual through insurance. Social insurance are:

- statutory pension insurance,

- health insurance,

- workers’ compensation insurance, and

- unemployment insurance.

Some social insurance benefits are based on work, others on residence in Finland. People who work have the right to certain benefits. Their levels depend on the earnings from work. Earnings-related pensions and allowances are such benefits.

Earnings-related benefits are financed through contributions that are proportionate to the wage and, partly, to the insurance risk. The basic unemployment allowance is financed by the State.

Residence-based benefits are the national pension, the guarantee pension and minimum allowances that are independent of earnings. Under certain conditions, all Finnish residents are entitled to these benefits. The minimum security is financed mainly through tax funds and tax-like fees.

Social insurance is also supplemented by various allowances and assistance, paid out for various reasons. The income support is the last resort.

Read more:

When a worker falls ill and is unable to continue working, the health insurance allowance covers initially part of the loss in earnings. Kela pays the allowance to workers aged 18–67 years after a qualifying period of nine weekdays. To get the allowance, the worker who has fallen in must have been working for three months before the disability began. New pension accrues for short-term periods of illness.

As a rule, workers are paid the allowance based on the Health Insurance Act for 300 days at the most. If the disability continues after that, they will get a temporary rehabilitation allowance from the pension scheme. If the disability is permanent, Kela and the pension providers pay out a disability pension or partial disability pension.

The worker can get rehabilitation to improve or restore their work and earnings capacity from either the earnings-related pension scheme or the national pension scheme.

Read more:

As a rule, all employees are covered by the statutory workers’ compensation insurance.

Persons whose work is not covered by the statutory workers’ compensation insurance can be insured voluntarily or by taking out a workers’ compensation insurance for self-employed persons with one of the pension providers.

Farmers are covered by the Accident Insurance Act for Farmers. Military injuries and service-related illnesses occurring in military service, non-military service and women’s voluntary military service are compensated under the Act on Compensation for Military accidents and Service-Related Illnesses. Accidents and service-related illnesses occurring in crisis management operations are compensated under the Act on Compensation for Accidents and Service-Related Illnesses in Crisis Management Duties.

The workers’ compensation pension is paid to the injured after the health insurance allowance period ends. To qualify for this benefit, the ability to work of the insured worker must have been reduced by at least 10 per cent due to an accident or occupational disease and whose earnings from work have decreased as a result.

If a worker is injured not as a result of an occupational accident but in a traffic accident, they get compensation for loss of income paid based on motor liability insurance.

Compensation paid based on accident and motor liability insurance are primary. That means that the insured person is primarily paid compensation based on the accident and motor liability insurance and will get an earnings-related disability pension only if the earnings-related disability pension is bigger than the compensation for loss of income paid based on the accident and motor liability insurance. New earnings-related pension accrues from short periods of accident and motor liability insurance compensation.

Read more:

The Employees’s Group Life Assurance is an insurance arrangement that the social partners have agreed on. When a worker dies, their family is paid a compensation based on this insurance. The compensation is paid regardless of the cause of death.

In addition, the surviving spouse and the children are compensated from the earnings-related pension scheme. That compensation is based on the deceased worker’s own earned pension. Kela pays out survivors’ pension from the national pension scheme to supplement the worker’s earnings-related pension.

Read more:

An unemployed job applicant who resides in Finland and who has worked before qualifies for an unemployment allowance. The unemployment allowance is paid for 500 days at the most. The basic allowance and the earnings-related unemployment allowance are paid under the same conditions.

To get the earnings-related unemployment allowance, the individual must be a member of an unemployment fund for a certain period of time. Earnings-related pension accrues also for periods of earnings-related unemployment allowance.

The labour market support secures the income for unemployed individuals who reside in Finland but who do not qualify for an unemployment allowance because they have no work history. In other words, the labour market support is intended for unemployed individuals who are entering the labour market for the first time. It is also granted to unemployed persons who have got the unemployment allowance for the maximum period of days (500 days).

If a self-employed person has been a member of an unemployment fund for the self-employed, they qualify for the earnings-related unemployment allowance or training. Otherwise they will get the basic allowance paid by Kela.

A person has the right to additional days based on the Unemployment Security Act if they have reached the age that qualifies for additional days before the maximum number of unemployment allowance days (500 days) are up. In that case, the unemployment allowance is paid until they reach their retirement age or until they turn 65.

For those born between 1957 and 1960, the age limit for additional days is 61 years and for those born between 1961-1962, it is 62 years. After that the age limit rises and is abolished completely for those born in 1965 or later.

The self-employed do not qualify for the additional days of the unemployment allowance. When the 500 days of the unemployment allowance are up, the self-employed may qualify for the labour market support.

Persons born before 1950 had the chance to retire on an unemployment pension as of age 60.

Read more: